As a self-employed chiropractor, you rely on bookkeeping essential to tracking profits, plan your practice’s future, and weather seasonal ups and downs in demand.

But that’s just the start of it. An organized bookkeeping system also helps you track and take advantage of tax deductions for chiropractic practices. And it can even increase your odds of securing a business loan or line of credit.

Think of this guide as a crash course in bookkeeping for your chiropractic practice. Bookkeeping can feel overwhelming at first. But once you get the hang of it, running your practice becomes less stressful, more profitable, and even—possibly—more fun.

{{resource}}

What is bookkeeping for chiropractic practices?

Bookkeeping is the day-to-day practice of recording every business transaction for your chiropractic practice. Each transaction appears in a document called the general ledger.

Today, most bookkeeping systems today are digital. But the general ledger was once literally a very large book where business owners (or their bookkeepers) made entries each time money was earned (revenue) or spent (expense).

For each entry in the general ledger, you’ll find:

- The transaction date

- The transaction amount

- Whether money was spent or earned

- The transaction account or sub-ledger (how the transaction is categorized)

Looking at your chiropractic practice’s general ledger, you get a complete history, in chronological order, of revenue and expenses.

That means you have a record for each time a client has paid you. You also have records of every time you spent money on deductible business expenses like rent, insurance, continuing education, equipment, or supplies.

What’s the difference between bookkeeping and accounting for chiropractors?

Bookkeeping and accounting are closely interconnected. Sometimes the two terms are used interchangeably—but they are really two separate activities.

With bookkeeping, you record financial data. With accounting, you analyze that data, using it to prepare financial reports, make business plans, and file taxes.

While financial statements technically fall under the umbrella of accounting, most bookkeeping software—and financial platforms like Heard—generate financial statements.

Financial statements (also called financial reports) take data from your books and use it to calculate important business metrics. For instance, a profit and loss statement (P&L) shows your revenue, expenses, and net income for a particular period—so you can track your chiropractic practice’s profitability over time.

The bookkeeping-to-accounting pipeline looks like this:

- Over the course of the financial year, you (or your bookkeeper) make entries in the general ledger.

- Each month or every three months, you generate financial statements that measure your practice’s performance.

- At the end of the year, you generate year-end financial statements summarizing business activity for the entire year.

- You bring your year-end financial statements, plus any necessary supporting documents, to an accountant. They use this information to prepare and file your taxes.

Accountants don’t only file taxes. You may go to an accountant for help restructuring your business, creating financial projections, and planning for growth.

When you use Heard, a team of professional bookkeepers imports and categorizes all your business transactions for you. The Heard Dashboard generates financial statements based on them. At the end of the year, your bookkeeping team hands off a year-end financial statement package to professional tax preparers who then file your taxes for you.

Is bookkeeping required for chiropractors?

There’s no law demanding you do bookkeeping for your chiropractic practice.

But bookkeeping is vital for monitoring your practice’s finances and accurately filing taxes. In fact, whether or not you keep up with bookkeeping could make or break your business.

You may just be starting out as a self-employed chiropractor. Even so, setting up some form of basic bookkeeping—for instance, with a spreadsheet—may increase your odds of success. It will also make running your practice less stressful and more efficient.

Other major benefits include:

Cash flow management

Making sure you have enough cash on hand to cover your business expenses isn’t always straightforward. That’s particularly the case due to insurance billing cycles and fluctuating revenue.

Bookkeeping shows where your money is being spent and how much you have on hand. That means you’re less likely to rely on credit to cover expenses, and less likely to go into debt.

Business insights via financial reports

Financial reports are the multi-tool of business admin, giving you the insights you need to:

- Cut costs

- Plan for growth

- Increase profits

- Reduce debt

- Expand your business

- Save for the future

- Reinvest in your business

Almost any decision you make that impacts your practice benefits from being informed by financial reports. And the only way to get financial reports is with good bookkeeping.

Tax preparation

At the end of the year, you or your bookkeeper or accountant generate financial reports summarizing all your business activity for the year.

Without these year-end financial reports, you may spend tax season playing catch-up, going back through your records to get all the information you need to file. That translates to wasted time and effort, plus a higher chance of making errors.

Also, when all your expenses in the general ledger are correctly categorized, you can see how much you spent on different expenses and use that information to file deductions.

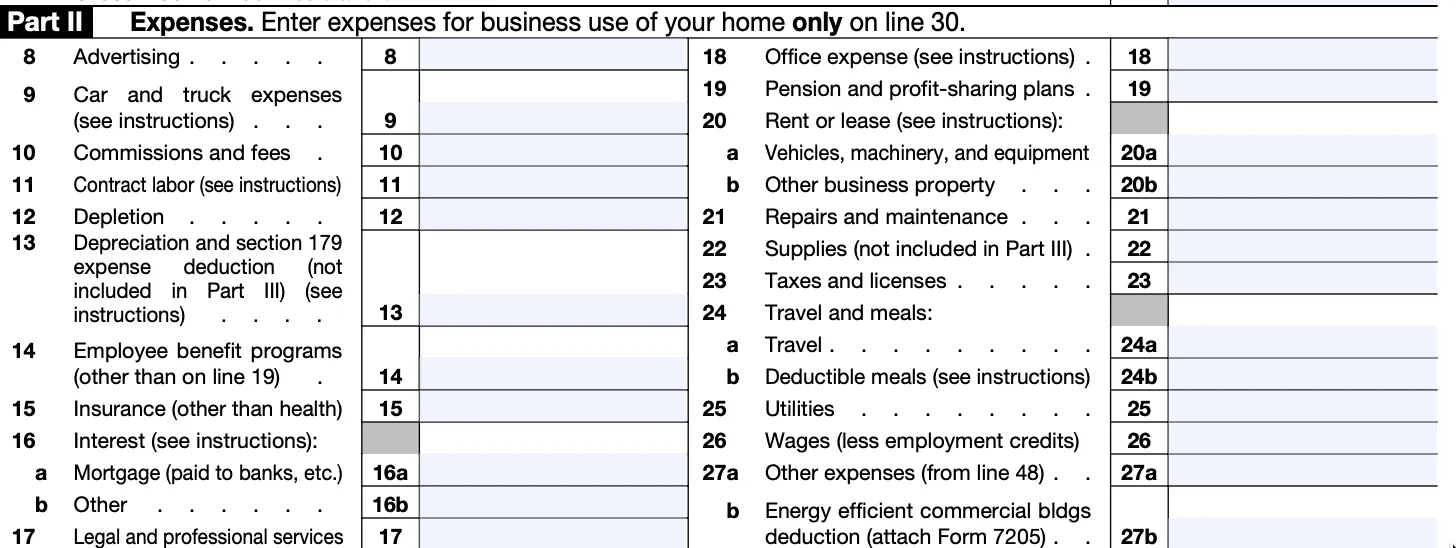

Here’s Schedule C of Form 1040, where businesses report their deductible expenses.

Without detailed records, it’s impossible to accurately complete this section of Schedule C. And every deduction you file means a smaller tax bill.

Securing capital

If you apply for a business loan, in most cases the lender—usually a bank or other financial institution—will ask you to submit financial records. They want to make sure your practice is sustainable and that you will be able to afford to pay back the loan. You can only get that data from a complete set of books.

Also, if you ever decide to sell your chiropractic practice or bring on investors, the other parties will expect a complete set of financial records for past years. And the farther back those records go, the better.

Buyers and investors want to see that your practice is profitable. They may also want to measure its growth trajectory and they can make their own plans for the future.

Long-term planning and growth

How would you like your practice to look like in five years? In ten? With data from your books, you can create financial projections to model future business performance.

That helps you plan for expanding your practice—by hiring employees, partnering with other chiropractors, or even just growing your client list. But it can also help you weather financial downturns.

Modeling best-case and worst-case scenarios helps you take steps now to ensure you are prepared for whatever comes later. That may include building up emergency savings, diversifying income streams, or limiting operating expenses. You can only make those moves when you have the kind of precise and accurate financial data bookkeeping provides.

{{resource}}

Bookkeeping systems for chiropractors

What does bookkeeping for your chiropractic practice look like on a day-to-day basis?

Your bookkeeping system is made up of the tools and/or professional support you use to prepare your books. Which system is best for you depends on:

- The size of your practice and its annual revenue

- Your knowledge and comfort level using different types of financial software

- How much time you are willing or able to devote to bookkeeping each week

These are the main DIY and professional solutions available you have to choose from:

DIY solution: Spreadsheets

Revenue: $0 – $20,000

Learning curve: Medium

Time commitment: High

If your total sales for the year come to $20,000 or less, your chiropractic practice’s finances are simple enough that you can manage them with a spreadsheet in Excel or Google Sheets.

A properly set up spreadsheet allows you to record transactions, organize them by date, and categorize each one.

Spreadsheets aren’t well-suited to double-entry bookkeeping (covered below), and making each entry by hand takes more time and effort than automatically importing transactions (other options allow this). Plus, if you plan to generate financial reports, you will have to do the math by hand.

But when your chiropractic practice is brand new and your transactions are few, a spreadsheet can serve as a stop-gap solution until you move on to something more comprehensive.

DIY solution: Software

Revenue: $20,000 – $50,000

Learning curve: High

Time commitment: Medium

Once your practice earns at least $20,000 per year, bookkeeping may become overly time-consuming. You’re now at the point where you can save time and effort with bookkeeping or accounting software.

The biggest benefit of accounting software is that, in most cases, it automatically imports transactions from your bank account. Each time you earn income or spend money on business expenses, the transaction appears in your general ledger. Then you categorize it by hand.

Accounting software almost always uses double-entry bookkeeping, and generates financial statements for you based on the data in your books.

One major caveat, however: expect a steep learning curve. If you’re new to accounting software, and especially if you’re new to bookkeeping in general, plan to devote time to following tutorials, taking notes, and logging practice hours before you can use the software with confidence.

Also, the information in your general ledger and financial statements is only as accurate as the data you enter. So, if you miscategorize a transaction, or if you forget to manually enter a transaction that occurred outside your banking account, software won’t catch the mistake. It’s up to you to get it right on your own.

Professional solution: Bookkeeper

Revenue: $50,000+

Learning curve: Low

Time commitment: Medium

If your practice earns $50,000 or more annually, there’s a good chance day-to-day bookkeeping with accounting software is too much work to be worth the time and effort. And, since your revenue is higher, you can now justify the expense of hiring a bookkeeper.

Professional bookkeepers work either at a firm or on their own as freelancers. Most use accounting software like QuickBooks to automatically import your transactions and categorize them for you.

That solves the problem of errors that could crop up when you categorize transactions yourself. You now have a professional working for you who guarantees your books are accurate.

But hiring a bookkeeper is not a complete hands-off solution. Your bookkeeper may still prompt you to categorize certain transactions they’re not sure how to categorize themselves. That’s especially the case if they lack experience working with chiropractic practices and aren’t totally familiar with your workflow, or with more complex parts of your business like the insurance billing cycle.

Typically, your bookkeeper will give you access to your books via whichever accounting software they use. That means learning the fundamentals of the software and keeping an eye out for any alerts that pop up.

Some bookkeepers work for firms that also employ accountants; your bookkeeper may be able to pass your books on to a colleague at the end of the year for tax filing. Otherwise, it’s up to you to hire your own accountant and bring them the financial statements your bookkeeper prepares.

Professional solution: Heard

Revenue: $50,000+

Learning curve: Low

Time commitment: Low

In some ways, using Heard is like hiring a professional bookkeeper.

Your bookkeeping team automatically imports transactions and categorizes them for you. You also have 24/7 access to your general ledger, financial statements, and other information.

One big difference: we built our financial platform specifically for chiropractors and other wellness practitioners. Your bookkeeping team trained in all the different forms of revenue and types of expenses chiropractors record on the books, as well as typical insurance billing cycles. that minimizes the number of transactions you need to categorize yourself.

In most cases, transactions are categorized instantaneously. Financial reports are generated up to the minute. You can access your Heard Dashboard any time and get access to all of your business’s important financial information, plus visual metrics measuring performance.

Finally, Heard handles tax filing for you—removing the need to hire an accountant.

At the end of each calendar year, your Heard team passes your financial statements on to professional tax preparers. They file your taxes for you. And since they specialize in serving wellness practitioners, they help you to take advantage of all the tax deductions available to chiropractors.

For a closer look, take a tour of Heard.

{{resource}}

Double-entry bookkeeping for chiropractors

Whether you use accounting software, hire a bookkeeper, or work with Heard, you will come face-to-face with double entry bookkeeping.

It’s the standard method of bookkeeping worldwide. With double-entry, each transaction appears on the books at least twice: first, as money entering or leaving an account; and again as money entering or leaving a different account.

Double-entry bookkeeping has been in use for over four hundred years—and for a good reason. Entering every transaction twice drastically reduces the likelihood of errors.

It may seem complicated at first, but once you understand a few basic concepts, double-entry becomes second nature.

Five types of accounts

Every account used in double-entry bookkeeping falls into one of five categories:

- Assets: Money (or equivalent) you have

- Liabilities: Money you owe

- Equities: Investment in your business (owner’s capital)

- Income: Money you earn

- Expenses: Money you spend

Each type of account behaves differently depending on whether it’s being debited or credited.

Credits and debits

For the time being, forget any notions you have about the meaning of “credit” and “debit.” When it comes to double-entry, these terms have nothing to do with plastic cards.

Each transaction on the books is entered once as a debit or credit and again as a debit or credit. As long as the debits and the credits for a transaction are equal, you’re good. If they’re not, it means you have an error somewhere in your books.

Debits and credits act differently depending on which category of account they’re debiting or crediting.

A double-entry example

If what you’ve read so far about double-entry bookkeeping has you scratching your head—don’t worry. The best way to get a sense of how the system works is through an example.

Example: You buy a new treatment table for your clinic. It costs $3,000. With double-entry, the transaction looks like this:

This entry simply shows that you’ve taken $3,000 in cash and turned it into $3,000 worth of chiropractic equipment.

Yes, double-entry bookkeeping can get more complicated than this. But do you need to know all the ins and outs of double-entry to start doing your bookkeeping? No.

Once you understand these fundamentals, you can build on them—whether you’re doing your own bookkeeping with accounting software or working with a professional.

{{resource}}

Cash basis vs. accrual accounting for chiropractors

There are two different methods for determining when you enter transactions on the book: the cash basis method and the accrual method.

Cash basis accounting is based on the exchange of money. You enter transactions on the book when money changes hands.

Example: Your internet provider sends you a bill for $80. One week later you pay the bill. The $80 is then entered as an $80 expense on the books.

Accrual accounting is based on when you charge someone money or when you incur an expense. It’s about business activity, rather than money changing hands. It doesn’t matter whether the payment has actually been made.

Example: Your internet provider sends you a bill for $80. As soon as you receive the bill, you enter it as a liability on the books. One week later, you pay the bill. Your cash account decreases by $80 (the amount paid), and your liabilities account increases by $80. Before, you had $80 in your liabilities account as a negative amount. Once you paid the bill, the $80 is wiped out by a positive amount—the $80 from cash.

Which method you choose depends on what is most straightforward for your practice and most accurately reflects the state of your finances. If you hire a professional bookkeeper, they can help you determine whether cash or accrual accounting is the best choice.

Accounts Receivable and Accounts Payable

If you plan to use the accrual method, you’ll be dealing regularly with Accounts Receivable (AR) and Accounts Payable (AP).

Following our example, the $80 you owe your internet provider is recorded as AP, or money you need to pay.

When you charge a client, the amount is recorded in AR as an asset—money that will be paid to you. As soon as your client pays, you remove the amount from AR and add it to your revenue account in the general ledger.

The general ledger for chiropractors

Your general ledger is the place you make all your bookkeeping entries. Each entry records:

- The date of the transaction

- The amount of the transaction

- The transaction account(s)

- The transaction category or categories

- Which accounts were debited or credited

Your general ledger may look different depending on which bookkeeping method you use (cash basis or accrual) and how you do your bookkeeping (spreadsheet, software, Heard, etc.)

Here’s an example for a chiropractor in private practice. To keep things simple, it uses single-entry bookkeeping. Single-entry is similar to the way transactions are recorded on your bank statement. Amounts in brackets are negative (e.g. expenses).

With this information, you can generate a financial statement—the P&L (covered below)—that shows you how much you earned in profit over a particular period.

When manually making entries into your general ledger, you or your bookkeeper assign income or expenses to the accounts listed in your chart of accounts.

{{resource}}

The chart of accounts for chiropractors

Your chart of accounts lists every account you use to label general ledger entries.

Each account falls under a specific category—income, expenses, assets, liabilities, and equity. These categories show up on different financial statements (covered below).

The chart of accounts differs from one business—and one chiropractic practice—to the next. It depends on your different types of income and expenses and which information you need to record. It may also depend on your typical expenses and the types of services you bill for.

Financial statements for chiropractors

Financial statements—also called financial reports—use the information in your general ledger to create documents summarizing important information about your practice.

A professional bookkeeper may generate financial statements on a monthly or quarterly basis. Financial platforms like Heard automatically generate up-to-the-minute statements based on the latest data in your general ledger.

For most businesses, two or three types of financial statements are key:

- Profit and loss statement (P&L): Also called an income statement, a P&L shows you how much your business has spent on expenses, how much it has earned as revenue, and how much it has kept as profit. It typically covers one month, one quarter, or the year to date (YTD). over a particular period.

- Balance sheet: This report shows you how much your business holds in assets, liabilities, and equity. It may be monthly, quarterly, or YTD.

- Cash flow statement: Exclusively used with the accrual accounting method, the cash flow statement reconciles the disparity between the income you’ve recorded on the books (e.g. Accounts Receivable) and the income you’ve collected (e.g. your Revenue account).

At the end of the year, you generate a P&L, a balance sheet, and a cash flow statement (if necessary) for the entire 12 month period. Your accountant uses the information on these statements to file your taxes.

A little more about each statement:

The profit and loss statement for chiropractors

The P&L calculates how much you’ve spent and how much you’ve earned, then subtracts your spending from your earnings to determine your profit (aka the “bottom line”).

A typical P&L lists all of your income accounts (e.g. Client Fees, Sales) and all of your expense accounts (e.g. Rent, Insurance, Utilities, Supplies) as line items.

Studying multiple P&Ls, you can find:

- Which expenses have the biggest impact on your profit (the bottom line)

- How much your income fluctuates from one reporting period to the next

- Your overall increase or decrease in profitability over time

The balance sheet for chiropractors

Your balance sheet lists your total equity, assets, and liabilities. By comparing your assets to your liabilities, you can see how much value your practice owns—in property as well as cash—compared to the debt it has to pay (in credit, loans, and other amounts owing).

You can also see how much of your own investment (or the investments of others) you’ve put into your practice in the form of owner’s equity.

Comparing balance sheets for different periods, you can see:

- How your assets have grown or decreased over time

- How your liabilities have increased or decreased over time

- The ratio of assets to liabilities, and how it changes

Also, by analyzing your balance sheet alongside your P&L for each reporting period, you will see the impact your income and expenses have on the amount of value your practice holds.

Finally, by comparing your liabilities (balance sheet) with your income (P&L), you’re able to calculate your debt-to-income ratio. This is an important measurement of performance financial institutions use when deciding whether to approve your business for loans or lines of credit.

The cash flow statement for chiropractors

Your P&L sums up the money your practice earns and spends. If you use the accrual method of accounting, you report both money you’ve charged clients as income (Accounts Receivable) and expenses you need to pay (Accounts Payable).

But since you enter those transactions when they’re incurred, and not when money actually changes hands, your P&L doesn’t accurately reflect how much cash you’ve earned and spent over a particular period.

The cash flow statement makes adjustments to your P&L so that the numbers you how cash has moved.

Your cash flow statements can tell you:

- Your liquidity, or how much money you have available to spend

- The effect of cash flow on your assets, liabilities, and equity

- Trends in cash flow, so you can anticipate ebbs and flows in cash and plan for the future

{{resource}}

Insurance bookkeeping for chiropractors

Billing insurance and recording it on the books isn’t significantly different from billing a client directly. There’s simply an extra account involved.

The Insurance Reimbursements account records income insurance companies pay out to you. It’s an income account, meaning it reports money your practice has earned.

If you use accrual accounting, your Insurance Reimbursements account connects with your Accounts Receivable. Remember, AR reports income you’ve charged for but haven’t collected as cash.

So, when you bill insurance, you record the amount under Accounts Receivable (as an asset). Then, when you receive payment, you move the amount to Insurance Reimbursements (as revenue):

The exact entry in your books will look slightly different depending on what type of bookkeeping system you use.

In general, however, you should make sure income in the form of reimbursements is labelled differently than income from cash pay clients. That way your P&Ls measure the impact of insurance reimbursements, as a distinct form of revenue, on your profits.

Bookkeeping best practices for chiropractors

If you have a bookkeeper working for you, or if you use Heard, the best practices you should follow are fairly straightforward:

- Make sure your bookkeeper has the information they need to do the books

- Answer any questions your bookkeeper may have about categorizing expenses

- Keep records of every expense you plan to claim as a tax deduction

If you do your own bookkeeping, it gets more complicated.

Here’s how you make sure your books are accurate and up to date:

Separate personal and business finances

Technically, this principle applies to any self-employed chiropractor, whether you use a professional bookkeeper or take the DIY approach. But most bookkeepers (including Heard) only work with clients who have already separated their personal and business activity into different bank accounts.

That’s because, if your business cash is mixed up with your personal cash, it can lead to serious errors.

So, the moment you go into business, open a separate business checking account (and, if necessary, apply for a separate business credit card).

That way, when your transactions are automatically imported into your bookkeeping system—or when you review your bank statements and manually enter transactions—there’s no question which transactions are for business and which are personal.

Also, if your chiropractic practice is registered as a limited liability company (LLC), you could compromise your limited liability by mingling personal and business finances (this is called “piercing the corporate veil.”) As a result, your personal assets may be on the line in case of debt collection, insolvency, or legal proceedings.

Reconcile the books

Reconciling the books is the practice of checking entries in your general ledger against information recorded in your bank statements.

Even if transactions are automatically imported into software (or into your bookkeeper’s system), mistakes may occur. Some transactions may not be imported, or they may be imported more than once. Refunds may not show up, or entries may be incorrectly categorized.

Also, bank charges—checking account fees, overdraft fees, and others—may not automatically import into your books.

At the end of each month, reconcile your books with your bank account. Think of it as financial hygiene. It’s part of regular bookkeeping best practices for every business.

Generate and analyze regular financial statements

When business is going well and you’re making healthy profits, you may be tempted to run your bookkeeping on cruise control and ignore your financial statements.

However, even if things are going well now, trouble may be brewing—for instance, in the form of stagnant cash flow, gradually increasing liabilities, or unnecessary expenses that eat away at your bottom line.

By making a habit of generating and analyzing your financial statements each month, you’ll always keep tabs on your finances—so you can catch problems before they become serious.

Even better, by looking at your statements and comparing them from one month to the next, you may discover ways to make your practice more profitable.

Catch up on bookkeeping when you need to

If you’ve fallen behind on bookkeeping, whatever you do—don’t procrastinate. Get caught up ASAP.

Falling behind can take the form of:

- Forgetting to import or manually enter transactions on the books

- Not bothering to generate financial statements

- Losing track of where money is going and where it’s coming from

Out-of-date books not only fail to give you the information you need to run your business well; the problem tends to compound over time.

Then, you may find that tax season has suddenly arrived and you lack the information you need to file and pay taxes. At that point, you’re in a much worse situation—facing potential IRS penalties—than you would be if you had simply gone back earlier and done the work to catch up.

If you’ve fallen behind on bookkeeping and the problem has grown to become overwhelming, contact a professional bookkeeper for help. Or get in touch with us here at Heard. We can catch up on your bookkeeping for you and keep it on track for the future.

{{resource}}

Common bookkeeping pitfalls for chiropractors

As well as keeping on top of bookkeeping best practices, you should learn to recognize the problems self-employed chiropractors most commonly run into when doing their books.

Here’s what you need to watch out for if you do your own bookkeeping:

Missing entries

An entry may be missing from the books because you forgot to make it, or else because your accounting software failed to import the transaction. In either case, it can create major problems later on.

Left undetected, missing entries may create discrepancies in your financial reports months later, even causing trouble when tax season rolls around.

The solution: Reconcile your books each month.

Miscategorizing entries

Particularly when you’re just starting out, you may make mistakes categorizing bookkeeping entries.

Minor errors—llabeling an insurance reimbursement as cash paid directly by your client, for example—may not spell immediate disaster. But they add up over time and lead to inaccurate financial statements that fail to reflect how your business is really performing.

The solution: Familiarize yourself with your chart of accounts and double check your entries.

Sticking with systems that don’t work

Chiropractors whose businesses are growing face a typical problem: they’re comfortable using spreadsheets or the accounting software they started their practice with, and stick with it even as their workload becomes unmanageable.

The stress from financial admin can spill over into other parts of their business, even leading to burnout.

If bookkeeping is causing you stress, start tracking how much time you spend on it each week. Then translate those hours into your hourly rate for client consultations. You can think of that amount as the cost of bookkeeping for your practice.

Then consider whether you’d be willing to spend the same amount (or less) in cash on a professional solution.

The solution: Remain flexible and open to new ways of managing your finances, and make the switch when the time is right.

Throwing out records

For every tax-deductible expense you claim, you must maintain records to back up the claim.

For instance, if you claim $24,000 in deductions on your taxes for office rent, you should have receipts from your landlord proving you paid all $24,000 over the course of the year. (A copy of your lease, plus bank statements, may suffice.)

If they audit your business, the IRS will ask for proof supporting all your claims. If you come up short, you could be on the line for the tax you originally deducted.

The solution: Set up a recordkeeping system and hold on to all proofs of purchase for at least three years or, ideally, six.

HIPAA compliance and bookkeeping for chiropractors

In order to remain HIPAA compliant, you must guarantee that none of your clients’ protected health information (PHI) is recorded in your bookkeeping system.

PHI includes any evidence that clients received care from you—including their names. Any software that stores your clients’ name must be certified HIPAA compliant, meaning it meets certain security standards for HIPAA.

If you use software like QuickBooks or Xero—or if your bookkeeper uses it—you are not using a HIPAA-compliant method for storing client data. Make sure client names and other information is not included in bookkeeping entries.

Also, if your bookkeeper—or your accountant, or any professional outside your practice—has access to information in your general ledger, and your general ledger includes your clients’ names, you’re in breach of HIPAA.

Whatever bookkeeping solution you use, follow these best practices:

- Avoid including client names or any other information in ledger entries (e.g. in notes or account names used to identify payment from clients)

- When you do need to refer to a particular client in your books, use a confidential client number

- Only invoice clients using HIPAA-compliant software, like your EHR

- Do not share clients’ names or personal details when discussing business with bookkeepers, accountants, tax preparers, or any other financial professionals

Is the cost of bookkeeping tax deductible for chiropractors?

Good news: any money you spend on bookkeeping software, hiring a bookkeeper, or using Heard is 100% tax deductible.

If you are a sole proprietor, you can report your total bookkeeping expenses for the year with Schedule C of Form 1040, on line 17 as “legal and professional services.”

(Other business entities, like LLCs filing as S corps, use their own tax returns to report deductible expenses.)

You can also deduct the cost of hiring accountants or tax professionals on the same line.

All of this helps to offset the cost of a professional bookkeeping solution for your chiropractic practice—a solution which will likely, when all is said and done, make your practice more profitable and easier to manage.

Key takeaways

- Bookkeeping is the practice of recording financial transactions for your chiropractic practice.

- A tax preparer (CPA or EA) uses your bookkeeping information (including year-end financial reports) to file your taxes.

- By keeping up with bookkeeping, you gain insight into how your business is performing and enjoy a simpler, easier tax season.

- Cash basis accounting only records when money changes hands, while accrual accounting records when income is earned or expenses incurred.

- The general ledger is where you record and categorize all transactions for your chiropractic practice.

- The three key financial reports are the P&L (measuring your profit), the balance sheet (measuring your assets, liabilities, and equity) and the cash flow statement (correcting discrepancies between accrual accounting records and cash on hand).

- For the sake of HIPAA compliance, your clients’ personal health information (PHI) or other information should never appear in the general ledger or in any other part of your bookkeeping system.

—

With Heard Bookkeeping, you get done-for-you monthly bookkeeping and easy-to-understand financial reports. Click here to learn more.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

Bryce Warnes is a West Coast writer specializing in small business finances.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.