This article is co-authored by Mentaya

When starting a therapy practice, therapists are faced with the question: Will I or will I not take insurance?

This decision boils down to three main options:

- Go in-network: get paneled with insurance companies, either through a company like Alma or on your own.

- Go out-of-network: only accept private pay clients.

- A mix: Go in-network with some insurances and take some private pay clients as well.

In this article we will talk about what it means to be an out-of-network provider (options 2 and 3).

Specifically we will:

- Explore reasons why some therapists choose this path.

- Explain how out of network billing works.

- Highlight resources available to out of network providers.

- Provide you with an extensive glossary of insurance terms.

{{resource}}

What is an out-of-network provider?

An out-of-network provider is not part of any insurance panels and they set their own fees. This is also called “private pay,” “cash pay,” or sometimes “fee-for-service.”

What a lot of people don’t know is that most preferred provider organization (PPO), point-of-service (POS), and high-deductible health (HDHP) plans have both in-network and out-of-network benefits. This means that even though you are out of network, many of your clients may be able to get reimbursed for therapy from their insurance company.

Why do therapists choose to be an out-of-network provider?

Top three reasons why therapists choose to be an out of network provider:

- More flexibility: You can choose your clients and run your practice the way you want – it is not controlled by insurance.

- Higher pay: Out-of-network providers can charge their full fee and avoid insurance companies taking a hefty cut of their pay.

- More time: Being out-of-network, you can avoid time consuming administrative tasks and paperwork required by insurance companies.

How do therapy clients typically get reimbursed for out-of-network therapy?

1. Client verifies their insurance benefits.

Clients often don’t know that their insurance plans may cover out-of-network services, despite them actively paying for these benefits.

To determine whether their insurance plan includes out-of-network benefits, and how much they can expect to get reimbursed, clients can reach out to their insurance company directly. Though this is not a difficult process, many clients never get around to making the call. As a result they may opt to go with an in-network therapy provider. Unfortunately, since there is such a high demand for therapists, this may result in waiting on long waitlists, or going with a therapist that is not a good match for the client.

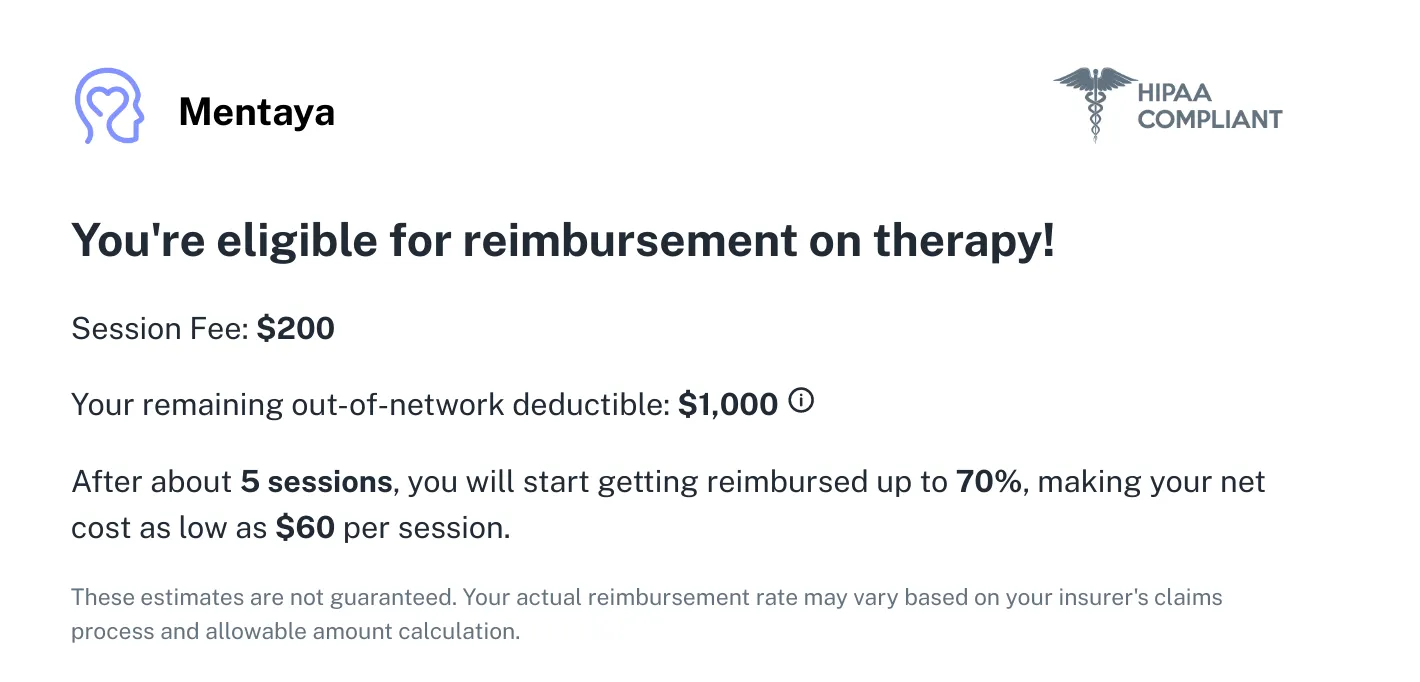

A growing number of therapists are using online resources, like Mentaya's benefits checker, to confirm how much clients can expect to be reimbursed by insurance. One provider explained: “I let my clients know I charge $200 per session and I don’t take insurance, but I do work with a platform that gets clients reimbursed. I let them know most of my clients get 70% of sessions reimbursed.”

For those with out-of-network benefits, reimbursements can range from 40-80% of therapy costs, significantly reducing session costs to a level comparable to a co-pay.

As highlighted by Mentaya’s benefits checker above, based on the provider’s session fee and their client’s remaining out-of-network deductible you can calculate how many sessions need to occur before the client will start to get reimbursed.

2. Therapists provide a superbill.

Clients need to submit a superbill or claim to their insurance company for therapy reimbursement. A superbill is a document that includes all necessary information required by insurance companies to process reimbursement for the services provided.

To generate a superbill, therapists can use their Electronic Health Record (EHR) software or create a template with the client's name, date of service, therapist's name and credentials (including their Tax ID or NPI number), diagnosis codes (ICD-10 codes), treatment codes (CPT codes), and fees charged for each service.

3. Client submits a superbill.

Clients will then submit the superbill to their insurance, either by uploading it directly to their insurance website or by mailing it. Sometimes the insurance company may not approve the superbill due to missing or incorrect information, insufficient documentation, or exceeding coverage limitations.

If done correctly, utilizing out-of-network benefits can serve as a bridge between in-network and out-of-network therapy, reducing the client's net costs while still allowing the therapist to get paid their full fee.

However, why does this still sound like so much work? Afterall, as an out of network provider you have ultimately made the decision to distance yourself from insurance companies.

{{resource}}

How to remove the frustration of dealing with insurance:

While it seems like a happy middle ground, all the insurance paperwork and responsibility is handed over to the client, who might not have the motivation, resources, and/or knowledge to complete the process properly.

Fortunately, companies like Mentaya exist to make the process easier, for both the therapist and their clients. They handle everything from instantly verifying benefits to automatically submitting claims, which helps therapists who want to be private pay, while saving clients up to 80% on therapy.

Outsourcing ways to help clients through companies like Mentaya can go a long way.

Nuts and bolts: key insurance terms

Here are some important insurance terms that therapists should be familiar with to help their clients understand what they mean.

Deductible: This is the amount a person has to pay out-of-pocket for health services before their insurance benefits kick in.

Premium: This is the amount a person pays every month for their insurance plan.

Out-of-pocket max: This is the maximum amount a person has to pay with their own money for covered healthcare services. Once this maximum is reached, the insurance company pays for 100% of all covered costs for the rest of the year. Deductibles, co-insurance, and co-payments count towards this maximum, but plan premiums and out-of-network care and services do not.

Co-payments: This is the amount a person pays for their health services. For example, if a session costs $100 and a person's deductible has already been paid, their co-pay may be only $20 for the visit.

Co-insurance: Basically, the same as co-payments but instead of a fixed dollar amount, it is the percentage of that amount. For example, if a session costs $100 and a person has a coinsurance rate of 20% after meeting their deductible, they would pay $20 for the session.

Superbill and claims: A superbill is a document that generates a claim to prove to the insurance company that services were necessary. A therapist can provide a superbill to their client, who can then file the claim with their insurance company.

Reimbursement: Insurance includes reimbursement policies in which a person may pay out of pocket for a service, but can receive money back after submitting a claim. Plans differ on their reimbursement policies, so it's important for clients to understand their individual benefits.

Allowable amount: This is the maximum amount an insurance company will pay for a specific healthcare service. Can also be known as eligible expense, payment allowance, or negotiated rate.

Timely filing limit: Another way to say the deadline for submitting a claim to an insurance company for reimbursement of a covered healthcare service. The time limit varies from 90-365 days, depending on the insurance plan.

Mentaya helps therapists attract and keep more private pay clients, while being a part of making mental healthcare more accessible. No paperwork, just meaningful work. Use the code HEARD for a 30-day free trial.

Visit our Therapist Tax Center and Tax Deductions for Therapists Hub for everything you need to know about taxes as a practice owner. If you're just starting out, here's everything you need to know about How to Start a Private Practice as a Therapist.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.