Electing S corporation status for your therapy practice gives you more control over how your income is taxed. But not all businesses are in a position to benefit from becoming an S corp.

Here are the signs to look out for before making the switch.

A quick refresher on S corporations

By default, when you go into business for yourself, the IRS considers you a sole proprietor. You report all your business’s revenue and deductible expenses on your personal tax return. You pay income tax on all your income based on your personal tax bracket, as well as the 15.3% self-employment tax.

When you elect S corporation status, you become a shareholder in your own corporation. (If you’re the only shareholder, you hold 100% of the shares.)

You pay income tax on the S corp’s income, but not self-employment tax. Only the money you earn as wages as an employee of your own S corp is subject to additional taxes, in the form of payroll taxes.

You can also earn money from your S corp in the form of shareholder distributions, which are not subject to payroll taxes, and as tax-free benefits like a health reimbursement arrangement.

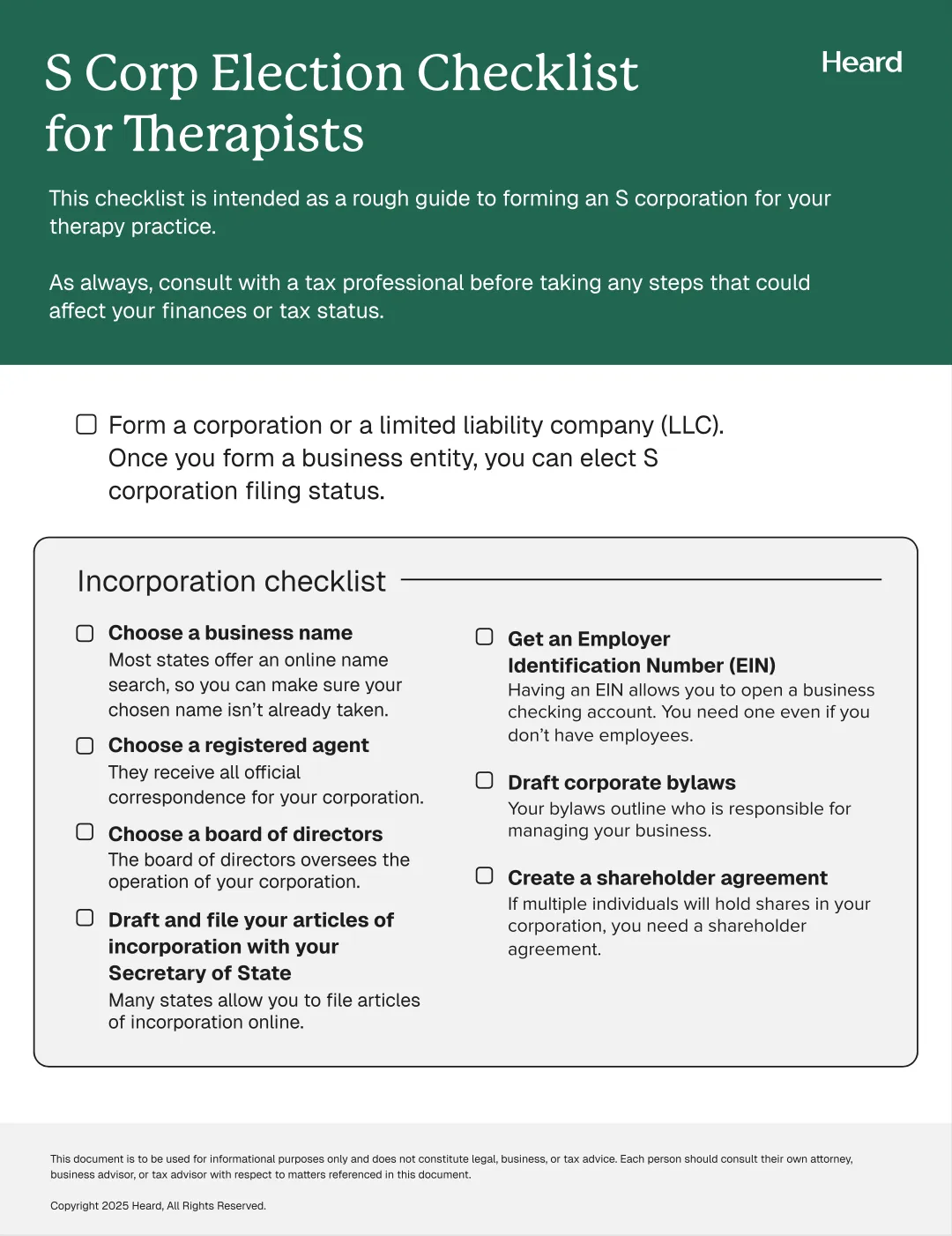

Most therapy practices that want to take advantage of S corp status first register as limited liability companies (LLCs) in the states where they do business. Then they elect S corp status by filing IRS Form 2553.

If you’re really new to the S corp concept, and all this talk about tax status and business entities has your head spinning, don’t worry: there’s a guide for that. Check out our Complete Guide to S Corporations for Therapists.

{{resource}}

When it’s worth the extra effort to lower your tax bill

Electing S corp status for your therapy practice can come with serious tax benefits, but it will cost you time, money, and effort.

We’ll cover the money aspect in the next section. For now, just be aware that it takes time and effort to elect S corp status. You either need to put some work in reading up on S corp elections and filling out forms, or hire an accountant to do it for you.

You’ll also have to set up payroll for your therapy practice, and your annual tax filing will become more complicated.

So, why do therapy practices elect S corp status at all?

One major reason: tax savings.

S corporation tax savings by the numbers

To better understand how businesses benefit from S corp status, we’ll compare how sole proprietorships and S corps are taxed.

Example 1: Sole proprietorship

Your therapy practice is a sole proprietorship, and your income for the year is $100,000.

As a sole proprietorship, you pay income tax and self-employment tax on 100% of your income.

Assuming you take the standard deduction and don’t make any retirement plan contributions, you’ll pay an estimated $14,260 in federal income tax at an effective tax rate of 16.6%, in accordance with 2023-2024 federal income tax rates.

But, since you’re self-employed, you must also pay self-employment tax. The self-employment tax rate is 15.3%, so you’ll owe roughly $15,300.

In total, you pay an estimated $29,560 in federal taxes.

Example 2: S corporation

Now suppose your therapy practice is an S corp, and your income for the year is $100,000.

You pay income tax on 100% of that, so you’ll owe the IRS an estimated $14,260 (just as you would with a sole proprietorship).

But you don’t owe self-employment tax. Rather, the income you’re paid by your employer (the S corp) is subject to FICA, which comes to 15.3% of your wages. Half of FICA is paid by the S corp, and the other half is taken out of your paycheck.

Your salary is $40,000. (The other $60,000 in income is either held by the S corp as cash assets, paid out in shareholder distributions, or paid out as tax-free benefits.)

Now, only that $40,000 salary is subject to FICA. The S corp pays 7.65%, and you pay 7.65%.

Once the dust settles, you’ve paid roughly $6,120 in FICA contributions, and an estimated $20,380 total in federal taxes.

Your total tax savings

Following these examples, you would pay $15,300 in self-employment tax as a sole prop. As an S corporation, you would pay $6,120 in total FICA contributions.

That’s a total savings of $9,180 for the year—nothing to sneeze at.

{{resource}}

You can afford the extra costs

As you can see, electing S corp status can save you a considerable amount in taxes. But it comes at a cost.

In order to make money, in this case, you really do need to spend it. Electing and then maintaining S corp status requires extra services—like bookkeeping and payroll—that cost money to outsource. And it may open you up to extra fees or taxes at the state level.

Before electing S corp status, add up all the fees involved and make sure:

- You can afford them upfront, in the case of one-time payments, and

- It makes long-term financial sense (ie. you aren’t paying more in fees each month than you are saving in taxes)

Here’s a breakdown of the extra costs that come with running an S corp:

One-time accounting fees

If you’re good with numbers and you love filling out IRS forms, you can form an LLC and elect S corp status with no extra help.

Otherwise, be prepared to hire an accountant. Working with an accountant, you can expect the cost for converting your sole prop into an S corp to range near the $1,000 mark.

Recurring accounting fees

The IRS pays closer attention to S corp tax filing than to sole proprietor tax filings, and S corps—in general—are more likely to be audited.

(That’s because many S corp owners try to take advantage of their business structure to underpay taxes.)

In order to avoid IRS trouble, you want your tax filing to be squeaky clean and correct. Typically, that means hiring an accountant to do it for you.

An accountant can also help you set a reasonable salary and plan shareholder distributions from your S corp.

For these services, expect to pay at least a few hundred dollars a year.

Bookkeeping

You can’t file taxes accurately unless you have accurate, up-to-date bookkeeping.

When you’re a simple sole proprietorship, you may be able to get by with a homemade spreadsheet and some back-of-napkin calculations. But with an S corp the DIY approach just doesn’t cut it.

The cost of hiring a bookkeeper varies widely. For more info, learn why bookkeeping is important for therapists.

LLC, PLLC, or other entity registration

In order to elect S corp status, you typically need to register as a business entity at the state level.

Not all states that allow businesses to form LLCs also allow therapists to form LLCs. In some states, therapists and others in medical fields must form professional LLCs (PLLCs) or professional corporations.

There’s usually a fee involved. For instance, in California, to register a professional corporation for your therapy practice costs a one-time fee of $200.

Local and state taxes

Depending on the state where you operate, registering a business entity may increase the amount you have to pay in local and state taxes.

For example, California charges businesses an $800-per-year franchise tax to maintain their professional corporation status.

Depending on local laws, you may also owe fees on the municipal or county level.

Insurance

Some types of business insurance for your therapy practice may increase their rates when your business structure changes. Also, different states have different laws about which types of insurance a registered business entity requires.

Payroll

Income tax and FICA withholding, reporting, and remittance add an extra layer of complexity to your month-to-month bookkeeping—even if you’re the only employee on payroll.

You’ll also need some form of employment agreement to make it official.

Many therapy practices outsource this work to a payroll provider. The monthly or annual cost of a payroll provider varies widely. As an example, for a company with just one employee on payroll, Heard’s partner Gusto charges $46 per month for payroll and benefits integration.

{{resource}}

You have the cash flow to cover it

Generally speaking, “cash flow” refers to the rate at which your business earns cash. The more frequently you’re paid by clients, the higher your cash flow.

In a more specific sense, it’s the rate at which your accounts receivable converts to cash—that is, how quickly clients who owe you money pay it.

In either case, your cash flow requirements are likely to change once you elect S corp status.

You now have new expenses to cover—like your own wage—on an ongoing basis. When your S corp doesn’t have the cash to cover those expenses, you’ll either need to dip into your savings or rely on credit.

Sole prop vs. S corp cash flow requirements: an example

Here’s a quick comparison demonstrating how cash flow requirements may differ depending on whether your business is a sole prop or an S corp.

Sole proprietorship

Suppose your monthly recurring expenses look like this:

You can technically withdraw money from your business checking account any time you need it for personal use. For the sake of keeping your bookkeeping organized, however, it’s best to set an owner’s draw—a certain amount you withdraw every month to pay yourself.

With this (simplified) arrangement, you need to have $5,000 positive cash flow each month to cover operating expenses.

S corporation

For an S corporation with the same office expenses, paying the same amount as the owner’s draw above as salary to the owner, monthly expenses would look like this:

Simply turning that $3,400 per month from owner’s draw to salary, and outsourcing your payroll, increases your cash flow requirements by $286.

That may not seem like much. But there’s an important difference between owner’s draw and salary: Your owner’s draw is optional. Your salary is not.

Suppose one month a few of your clients miss their appointments, and your revenue for the month is $300 short.

That’s alright—you can always reduce your owner’s draw by $300. There’s no law forcing you to take the same draw every month.

While it’s good to stay consistent for the sake of planning and keeping your books organized, a $300 dip in owner’s draw for the month is no big deal.

Now suppose you’re $300 short in cash, and it’s time cut yourself a paycheck. Problem is, you can’t just reduce your salary. You need to be paid your full wage; if you don’t have cash to cover the full amount, you may be able to delay a few days, or carry forward the difference to your next paycheck—but that introduces all kinds of payroll and bookkeeping headaches.

At the end of the day, if you’ve hired yourself as an employee receiving a $40,800 salary, you need to pay yourself that salary. There’s no wiggle room.

The bottom line with cash flow

Once you elect S corp status, everything about your accounting, bookkeeping, and tax filing becomes more complex. In some ways—like the need to cut yourself a regular paycheck—it becomes more rigid.

The potential long-term tax savings are significant, but you need to make certain you can cover your costs month to month.

You’re in business with your spouse

One final, possibly niche indication it’s time to elect S corp status: You’re planning to hire your spouse.

When your therapy practice is an S corporation and you hire your spouse, there are potential tax savings to be had by both your business and your significant other.

Federal law does not require you to pay your spouse minimum wage. Instead, you can compensate them with tax-free health benefits. Plus, because you’re married, you can transfer non-wage funds to them without being taxed.

There are a number of factors to take into account here—not least of which is how to pay your spouse a reasonable wage, even if you’re paying them in the form of health benefits. For a deeper dive, check out our guide to employing family members at your therapy practice.

—

Electing S corp status can net you serious savings on your tax bill provided you take into account the extra expenses involved. Before you make any major decisions, be sure to consult with a financial professional, and check out our Complete Guide to S Corporations for Therapists.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

Bryce Warnes is a West Coast writer specializing in small business finances.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.

Lock in our lowest prices of the year, plus exclusive add-ons. Sign up by December 31 to take advantage of these savings.

Schedule a free consult