Your therapy practice’s balance sheet is a snapshot of what your business is worth. It tells you how much you have (assets), how much you owe (liabilities), and your stake in the business (equity).

Keeping an eye on your balance sheet can help you track your practice’s growth, make plans for the future, and anticipate bumps in the road ahead.

Along with your profit and loss statement (P&L), it forms the core of financial reporting for your business.

The fun part? Balance sheets are pretty easy to read. If you can interpret your monthly bank statement, a balance sheet for your business isn’t difficult.

By the end of this article, you’ll know everything you need to know about your private practice’s balance sheet.

{{resource}}

Why is it called a balance sheet?

Traditionally, a balance sheet is split into two halves:

- The left side, which includes your company’s assets

- The right side, which includes your company’s liabilities and equity

The balance you’re looking for on your balance sheet is the balance between the left and right bottom lines. Your total assets should be equal to your total liabilities and equity.

The reason for this will make more sense once we dive into assets, liabilities, and equity. (What does the balance sheet tell you?)

When the left and right sides do not balance each other out, your balance sheet isn’t accurate. That could be due to:

- Bad math

- Not listing all assets, liabilities, and equity

- Using information from different time periods (eg. A bank balance from the beginning of the month, and an Accounts Payable from the end of the month)

If you’re creating your own balance sheets, and they consistently fail to balance, it could be a sign you need bookkeeping support for your therapy practice.

Your balance sheet vs. your profit and loss statement

While a P&L tells you how much money your business earned or spent within a specified period, a balance sheet tells you how much money your business has as of a particular date.

For instance, you can look at a P&L for the month of March, and see what your business spent on expenses like rent and utilities between the dates March 1 and March 31st. You’ll also see what you earned—from client bills, and other revenue streams—during that time.

But nowhere on your P&L will you see how much money you have in the bank, or how much you owe in debt. That’s where the balance sheet comes in.

A balance sheet for March 31st will tell you exactly where your business stands. And your P&L for March 1st to March 31st will tell you how you got there.

What does the balance sheet tell you?

The information on your balance sheet is broken down into three categories: assets, liabilities, and equity.

Assets

Assets include everything your practice owns and uses to generate revenue.

Some assets, like cash, stocks, and bonds are financial assets.

Non-financial assets are categorized as either tangible or intangible.

Tangible assets are easy to convert to cash value. Examples of tangible assets include accounts receivable (money owed to you by clients), your work computer, business signage, and office furniture. All of these can have a cash value assigned to them.

Intangible assets are harder to assign a value to. Examples of intangible assets include your reputation, copyright on a book you wrote, or your business name. While all of these have value, it’s difficult to say exactly how much each is worth in cash.

Finally, every asset in these three categories is either a current or a fixed asset.

A current asset is one you expect to convert into cash within one year. Accounts receivable is a good example. Since you will (hopefully!) be paid by your clients within one year, the amount owing is considered a current asset.

A fixed asset is one you don’t expect to convert into cash within one year. Your work computer is a good example of a non-current asset.

Typically, fixed assets make up the material backbone of your practice—the stuff you need in order to keep your business running. Current assets make up your revenue streams and the cash you have on hand.

Liabilities

The liabilities category on your balance sheet includes all the debt your practice owes.

Each liability is categorized as either current or long-term, meaning you expect to repay it within one year or you expect to repay it in more than one year, respectively.

Some common liabilities for a therapy practice include:

- Small business loans

- Business credit card debt

- Money owed to contractors (accounts payable)

- Money owed to employees (payroll)

- Utility bills

- Rent

- Tax payments owing

Equity

Equity is your stake in the company—money that you would personally claim in the event you shut down your practice and sold off all your assets.

For a therapy practice, the equity section of the balance sheet typically includes just two items:

- Owner’s equity, the initial investment the owner used to start their business.

- Retained earnings, the money the business has earned and saved.

On most balance sheets, equity and liabilities are added together in one final line item: Total Liabilities and Equity.

In the event you shut down and liquidated your business, you’d pay all the debts you owe. You’d also pay yourself the equity you own in the business. If you own 100% of your practice, that means 100% of your practice’s assets, after covering your liabilities (your net assets).

{{resource}}

Where do balance sheets come from?

You have a few options when it comes to generating balance sheets for your therapy practice.

- Do it yourself. By referring to your income statements, your general ledger, and your bank and credit accounts, you can create your balance sheet.

- Use software. Basic accounting software can generate balance sheets for you, so long as your bookkeeping is up to date and accurate.

- Hire a bookkeeper or accountant. A bookkeeper or an accountant can deliver balance sheets on a regular basis. This is the priciest option.

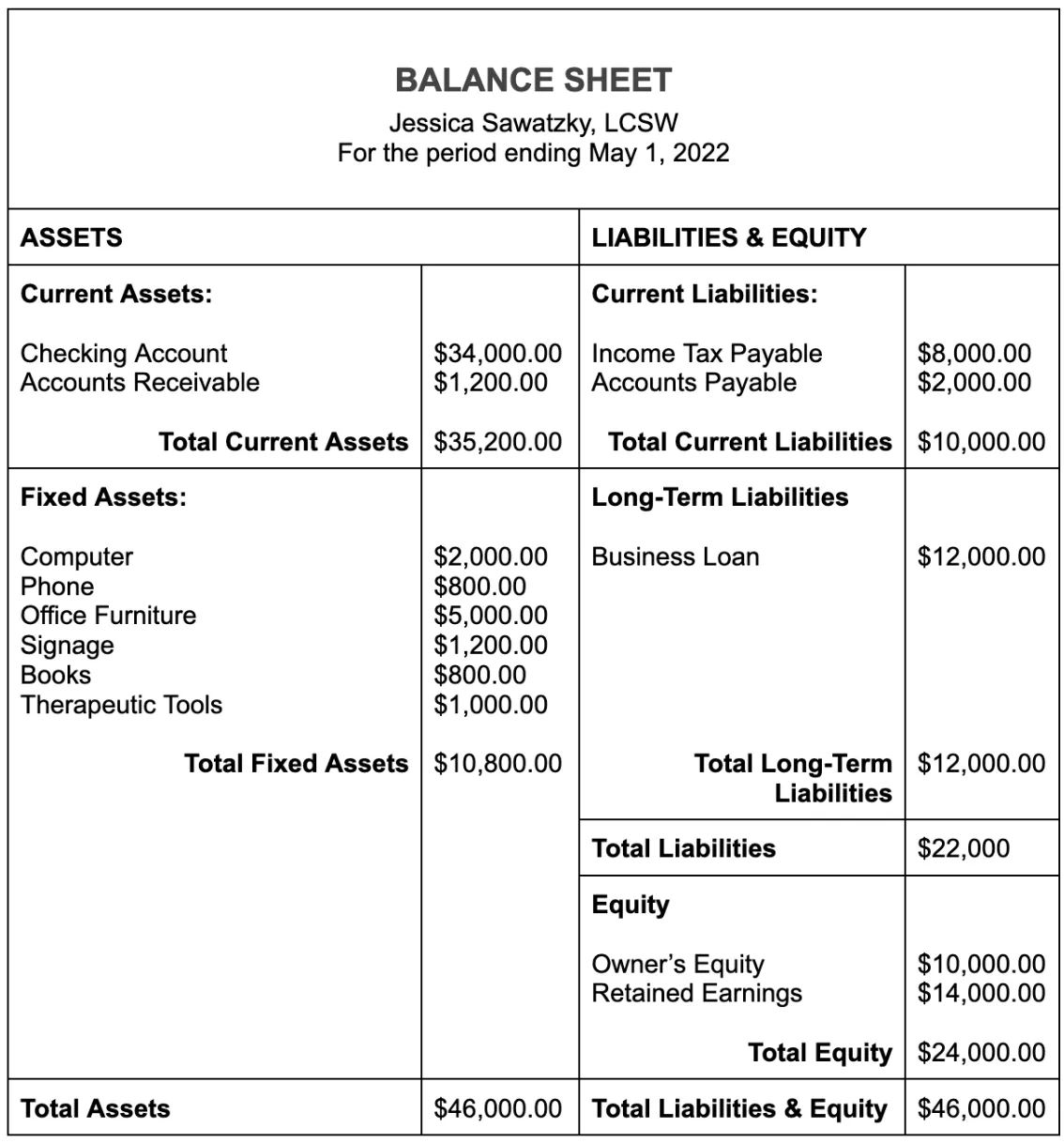

Example balance sheet for a therapy practice

Now that you understand assets, liabilities, and equity, and how they work together, you have all the background knowledge you need to read your balance sheet.

Here’s an example of a balance sheet for a small therapy practice:

For the sake of simplicity, this balance sheet omits depreciation. Depreciation measures how the value of some items—like computers or office furniture—decreases over time.

You may notice that only the bottom lines (Total Assets and Total Liabilities & Equity) match up. The other line items aren’t equivalent.

For instance, looking at the Business Loan liability of $12,000 on the right side, you won’t find its exact equivalent on the left.

That’s because the $12,000 has been used. Some of it may have gone into the bank (Checking Account), where it will later be used to cover expenses. Some of it may have been spent on fixed assets, like the Computer and Office Furniture line items. The money borrowed is part of your business—it’s just changed shape.

—

In order to unlock the true power of your balance sheet, you need to combine it with your P&L. Learn more about profit and loss statements for your therapy practice.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

Bryce Warnes is a West Coast writer specializing in small business finances.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.