If you run your own therapy practice, there’s a good chance you can lower your tax bill by claiming the Qualified Business Income (QBI) deduction.

The QBI deduction lets you write off up to 20% of your business income. But there are limitations you should familiarize yourself with before trying to claim the deduction.

Here’s everything you need to know about the QBI deduction, and how your therapy practice can benefit.

{{resource}}

What is the QBI deduction for therapists?

The QBI deduction was introduced as part of the Tax Cuts and Jobs Act (TCJA). Its effective start date was December 31st, 2017. In 2025, it was permanently extended under the One Big Beautiful Bill Act.

You can only claim the QBI deduction if you are self-employed and your business is a pass-through entity—that is, a:

- Sole proprietorship

- S corporation

- Partnership

- LLC filing as either a sole prop, partnership, or disregarded entity.

The amount you’re able to deduct by claiming QBI is based on your qualified business income. Not all business income counts as qualified.

What counts as qualified business income?

Your QBI is your taxable income for the year after claiming itemized or standard deductions and business expense deductions.

Not all income is qualified, however. Non-qualified income includes:

- Wage earnings (money made as a W-2 employee)

- Capital gains or losses

- Commodities transactions

- Foreign currency gains or losses

- Certain dividends, or payments in lieu of dividends

- Earnings received as reasonable compensation from an S corporation*

- Earnings received as guaranteed payments from a partnership

- Payments you receive as a partner in your business for services outside your capacity as a partner

- Qualified dividends from real estate investment trusts (REIT)

- Qualified publicly traded partnership (PTP) income

- Any earnings you’re otherwise unable to list as income on your tax return

- Any earnings not attributable to your business**

* This means that if your practice is an S corporation and you pay yourself a reasonable salary, you can’t deduct both the total income of the S corp and your earnings (double dipping).

** For instance, if you earn extra cash selling handmade jewelry on Etsy, you can’t claim it as QBI for your therapy practice

Broadly speaking, any income you earn in your capacity working at the principal trade of your business—in this case, acting as a therapist—amounts to QBI.

{{resource}}

Do therapy practices qualify for QBI?

Here’s the thing: Technically, if your business is a Specified Service Trade or Business (SSTB), you don’t qualify for the QBI deduction.

And technically (there’s that word again) a therapy practice counts as an SSTB.

But the IRS allows a major exception to SSTBs which—given the average income of therapy solo practices according to the 2025 Financial State of Private Practice Report—will likely let you claim the deduction.

Let’s back up a bit.

What is an SSTB?

The IRS provides a list of SSTBs. It includes businesses in the fields of:

- Health (including psychologists)

- Law

- Accounting

- Performing arts

- Consultancy

- Athletics

- Financial services

- Brokerage services

- Investing and investment management

- Trading or dealing securities and commodities

It also includes any business whose income depends on the reputation or skills of its owners or employees.

So, even if you are—for instance—a life coach and not a psychologist, your business likely still qualifies as an SSTB.

Luckily, that’s not a big deal.

The great big exception to the SSTB rule

Actually, there are two exceptions to the SSTB rule.

- If your taxable income before QBI is $182,100 (single) or $364,200 (married filing jointly) or less, your therapy practice is treated as a qualified business and not an SSTB

- If your taxable income before QBI is between $182,100 and $232,100 (single) or $364,200 and $464,200 (married filing jointly), you can claim a partial deduction

It’s more or less a limit on how much you can deduct if you have a therapy practice earning less than $220,050 per year, with the majority of filers able to claim the full deduction.

Note that these limits are for the 2023 tax year, and may change from one year to the next.

{{resource}}

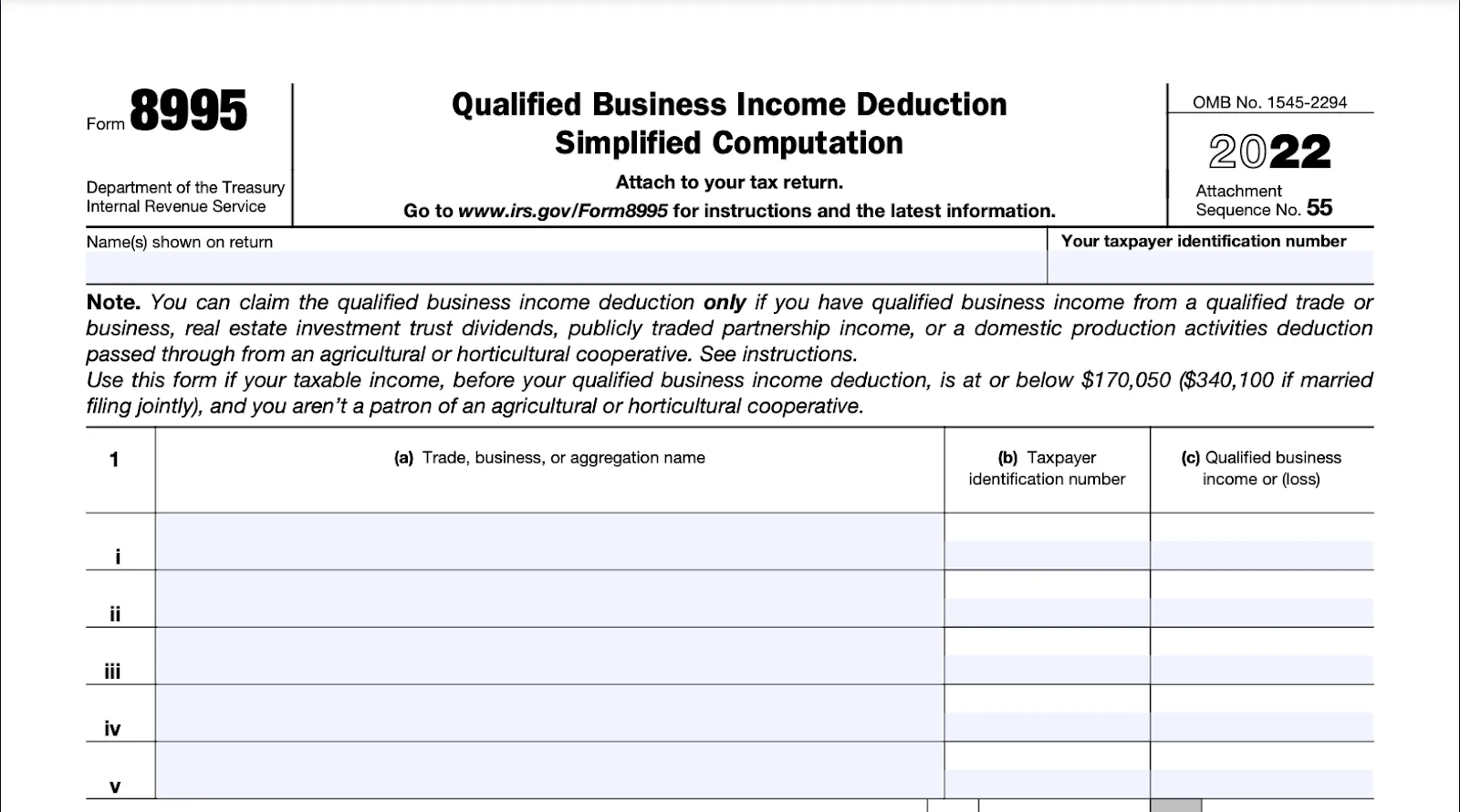

How to claim the QBI deduction for your therapy practice with Form 8995

Before claiming the QBI deduction, you need to calculate your qualified income.

Remember, your qualified income is your total taxable income for the year after applying either the standard or itemized deductions, as well as business expense deductions (write-offs for your therapy practice).

Once you determine your QBI, you must fill out and file either Form 8995 (if your QBI is equal or less than $182,100 (single) or $364,200 (married filing jointly)) or Form 8995-A (if your QBI is more than $182,100 (single) or $364,200 (married filing jointly)).

The good news about Form 8995 is it’s fairly straightforward. Once you’ve calculated your QBI and understand the income limits covered above, completing the form comes down to doing some simple arithmetic.

That being said, if part of your income comes from investments, or you’re doubtful for any reason whether all your income is qualified, consult with an accountant.

Given the fact that the QBI deduction has the potential to drastically lower your tax bill, and some of the complexities involved, it’s wise to get an expert’s opinion.

—

Looking for more ways to reduce your tax burden? Check out our complete list of tax deductions for therapists.

Visit our Therapist Tax Center and Tax Deductions for Therapists Hub for everything you need to know about taxes as a practice owner. If you're just starting out, here's everything you need to know about How to Start a Private Practice as a Therapist.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

Bryce Warnes is a West Coast writer specializing in small business finances.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.