Claiming deductions for your therapy practice reduces your tax burden. But in order to benefit, you need to understand which expenses qualify, where to deduct them on your return, and how to keep accurate records so you won't run into trouble in the event of an audit.

Consider this your complete guide to tax deductions for therapists—including the difference between tax deductions and credits, the latest changes to tax deductions for 2025, and how to take advantage of deductions before the end of the fiscal year.

But first, the basics.

What is a tax deduction for therapists?

Your therapy practice benefits from a tax deduction when you report a deductible expense on your tax return. A deductible expense is any cost you incur in the course of doing business that can be wholly or partially deducted from your taxable income.

On your tax return, you report your gross revenue or income, then subtract your deductible expenses to find your taxable income. Your federal income tax and self-employment tax are calculated as percentages of your taxable income. The rate at which your income tax is calculated depends on the amount of your taxable income and which tax brackets it falls under.

State and municipal taxes are also based on your taxable income. These vary from state to state and locality to locality. This guide mostly focuses on federal taxes.

Net income vs. taxable income

The terms "net income" and "taxable income" are sometimes used interchangeably. In reality, your net income, as reported on your annual profit and loss statement (P&L), may be a different amount than your taxable income.

That's because not all business expenses are 100% deductible. For example, you may only deduct 50% of the cost of qualifying business meals from your taxes. As another example, depending on the calculation method you use, the total amount you are able to deduct in home office expenses from your taxes may be less than the amount you actually spend on your home office.

Business deductions vs. personal deductions

Business expenses you deduct are different from tax deductions on your personal return.

That applies regardless of your business structure: When you are a sole proprietor, your person and your business are identical for tax purposes. But your personal deductions and your business deductions are reported on different forms.

There are two types of personal deductions. Above-the-line deductions determine your adjusted gross income (AGI). Other personal deductions—plus business deductions, if your business is a pass-through entity—are then subtracted from your AGI to determine your total taxable income.

Above-the-line deductions include retirement savings contributions, student loan interest, and medical expenses. They are calculated on Schedule 1 of Form 1040.

Itemized deductions (or the standard deduction) are subtracted from your AGI after above-the-line deductions have been applied. You can choose either to itemize these (calculate and report each deduction) or claim the standard deduction (a flat rate based on your marital status and whether you are filing singly or jointly).

Itemized deductions include charitable contributions, investment losses, and certain educational expenses.

In contrast to above-the-line and itemized deductions, business deductions are based on the expenses you incur running your business. They are reported and calculated on Schedule C of Form 1040, and then subtracted from your AGI after itemized deductions (or the standard deduction) have been applied. You can only deduct business expenses on your personal tax return if you are a sole proprietor.

The 2025 and 2026 standard deductions

When you claim personal deductions on your tax return, you can choose to either:

- Itemize, claiming each deduction

- Claim the standard deduction, a flat rate deduction available to all individuals regardless of income level

For the 2025 tax year, the standard deduction is:

- For those who are married filing jointly: $31,500

- For single filers and those married but filing separately: $15,750

- For heads of households: $23,625

For the 2026 tax year, the standard deduction is:

- For those who are married filing jointly: $32,200

- For single filers and those married but filing separately: $16,100

- For heads of households: $24,150

Tax deductions vs. tax credits

Tax deductions and tax credits for therapists both reduce the amount you pay in taxes, but they operate differently.

Tax deductions reduce your total taxable income—you deduct them from your AGI and the resulting amount is used to determine the taxes you owe.

Tax credits, on the other hand, are subtracted directly from the amount owing. For instance: if, based on your income, you owe $25,000 in federal taxes, and you qualify for a $1,000 tax credit, the amount you owe is reduced to $24,000.

How to qualify for business tax deductions

Any business or self-employed individual may claim tax deductions. But that doesn't mean you are free to deduct any expense from your taxes.

First, the expense must be ordinary and necessary. Second, before you claim it on your taxes, you should make sure you have a suitable record of the expense.

Ordinary and necessary expenses

In the words of the IRS: To be deductible, a business expense must be both ordinary and necessary. An ordinary expense is one that is common and accepted in your industry. A necessary expense is one that is helpful and appropriate for your trade or business. An expense does not have to be indispensable to be considered necessary.

To break that down:

- For an expense to be ordinary, it should be common in your industry.

- Example of an ordinary expense: A computer microphone so you can better treat clients via telehealth.

- Example of non-ordinary expense: Guitar lessons, in case you decide to record an album about your experiences as a therapist.

- For an expense to be necessary, it should be helpful and appropriate, and not extravagant.

- Example of a necessary expense: A mid-range computer microphone sufficient for telehealth, costing about $100.

- Example of an unnecessary expense: A home recording studio costing about $8,000.

The IRS is on the lookout for business owners writing off personal expenses as business expenses. Keep that in mind when planning your purchases.

Tax deductions and recordkeeping

For any expense you deduct that totals $75 or more, keep receipts or other proof of purchase on your records.

Keep the total amount in mind. A $100 computer microphone is a no-brainer—you should keep the receipt. But small purchases can add up to a large total. Coffee with business associates may cost only $10. But if you meet eight times over the course of the year, that brings your total deduction to $80. If you claim it, plan to have receipts to back it up.

In the event of an audit, the IRS can request receipts to back up your past three years of deductible expenses. If they suspect fraud, they can request another three years' receipts—for a total of six years' worth of financial records.

If during an audit you can't provide a receipt proving you paid an expense, you will be required to pay the difference—the amount you wrote off your taxes for the purchase—to the IRS. You may also be required to pay penalties.

How to file tax deductions

Tax deductions are filed as part of your regular federal tax return, and they are used to determine your taxable income. Which forms you file—and their deadlines—depend on your business structure.

Tax deduction schedules and forms

- Sole proprietors: Deduct your expenses from your gross income to determine your net income on Schedule C of Form 1040. This amount flows to Schedule 1, line 3 ("Business income or loss") and then to Form 1040, line 8 ("Other income") where it is included in your total income. You also report this amount on Schedule SE, where self-employment tax is calculated.

- S corporations: Your S corporation deducts its expenses from its gross income on Form 1120-S. Your share of the S corp's total net income is reported on Schedule K-1. This amount flows through to Schedule 1 and then line 8 of Form 1040.

- Partnerships: The partnership deducts its expenses from its gross income on Form 1065. Your share of the partnership's net income is reported on Schedule K-1, which you then enter on Schedule 1 and then line 8 of Form 1040.

- C corporations: A C corp deducts expenses from its gross income on Form 1120. Its net income does not pass through to shareholders. Instead, shareholders may receive dividends on stock they hold, or they may be paid an income as employees of the corporation.

Tax deduction filing deadlines

Tax deductions are filed as part of your annual business tax return.

- Sole proprietorships and C corporations: April 15th, or the next business day if April 15th falls on a weekend or holiday.

- S corporations and partnerships: March 15th, or the next business day.

Deductions and quarterly estimated taxes

If your business is expected to owe $1,000 or more in federal taxes, the IRS typically requires you to file quarterly estimated taxes.

If you underpay your taxes—if your total payments amount to less than what you owe—the IRS may charge you interest on the unpaid amount. You can avoid this penalty by following the safe harbor rule, paying either:

- 90% or more of the amount you owe for the current year; or

- 100% of what you paid last year (110% if your AGI is $150,000 or greater)

Keep in mind that overpayment can also be a problem, particularly in years when your total tax burden is less than it was in the past.

Deductions because of increased expenses or large purchases may lower your tax bill. That's a good thing, but it's important to adjust your estimated payments to account for it.

Some steps you can take:

- Check P&Ls against last year's reports. If you're following the safe harbor rule by paying 100% of what you owed the previous year, compare your monthly P&Ls with your P&Ls from the same months in the previous year. It will help you spot trends such as lower taxable income in the current year, and adjust your payments accordingly.

- Make projections for changing expenses. Rent increases, new software or SaaS subscriptions, continuing education, and large purchases like office computers or furniture can all put a dent in your taxable income. If you're anticipating these expenses, or if your monthly expenses have increased, create projections to estimate how they will impact your tax burden.

- Make a "true up" payment in Q4. Your fourth quarterly tax payment is due the January after the end of the tax year to which it applies. Once you close the books for the year, you should have a year-end P&L that tells you your total taxable income. You can use this amount to calculate your total tax burden, then adjust your fourth quarterly payment so that the sum of all four payments matches what you owe.

2025 tax deductions for therapists

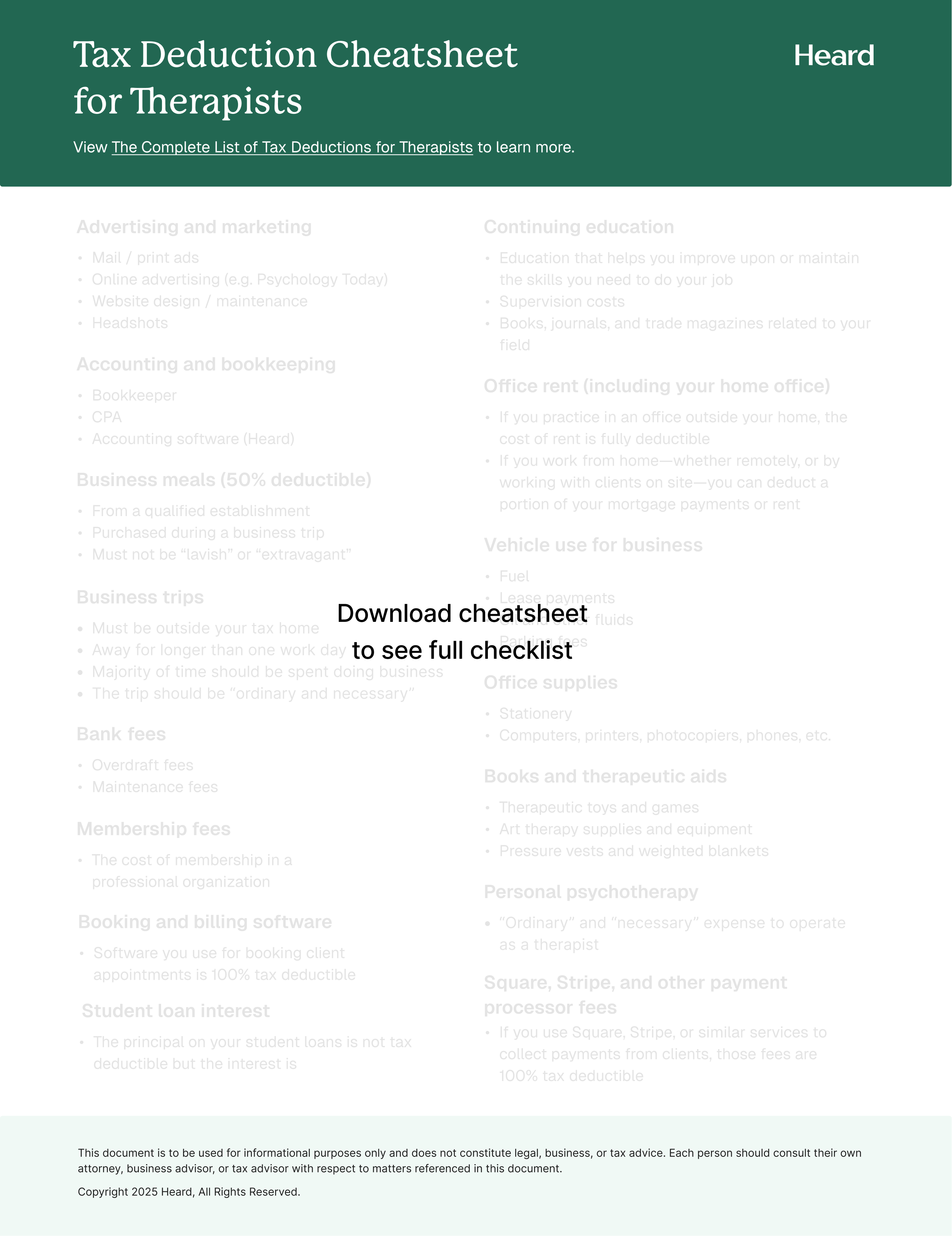

For a full list of tax deductions your therapy practice may qualify for, check out Therapy Practice Tax Deductions for 2025.

Here are the changes you should be on the lookout for in 2025:

The increased standard deduction

The standard deduction for individuals has jumped from $15,000 to $15,750. That may not be an earthshaking change, but it could affect how you make your personal deductions. If you typically itemize your deductions, recalculate them this year to make sure you're saving more by itemizing than you would by claiming the new, higher standard deduction.

State and local tax (SALT) deductions and pass-through entity tax (PTET) protection

The SALT deduction is an above-the-line writeoff that lets you claim state and local taxes as expenses, reducing your total federal tax burden.

The "One Big, Beautiful Bill" (OBBB) signed into law in July 2025 has increased the cap on this deduction from $10,000 to $40,000. (It's scheduled to return to $10,000 in 2029.) If you haven't claimed this deduction in the past, now would be a good time to start.

Also, the OBBB now federally protects PTET. After the $10,000 SALT cap was introduced by the federal government in 2017, many states introduced PTET. This was an alternative form of state-level tax that pass-through entities like sole proprietors and S corporations could elect to pay.

PTET is not subject to the SALT cap. So, in prior years, if your business's state and local taxes totalled more than $10,000, and your state offered PTET, you could choose to pay PTET instead of normal state and local taxes. Then, you could write PTET off as a business expense on your tax return. This loophole allowed businesses to avoid the SALT cap and claim bigger deductions.

There was always a danger that the federal government would step in to close the PTET loophole. But as part of the OBBB, states are guaranteed the right to offer PTET—so there's no longer a threat of it going away.

Now, if your total state and local taxes exceed $40,000—the new SALT cap—and your state offers PTET, you can reliably count on paying PTET and getting around the cap. It makes tax planning a little more straightforward for your practice, particularly if your state charges high taxes.

Telehealth tax deductions for therapists

When you treat clients via telehealth, these are the expenses you may be able to deduct on your tax return.

Multi-state deductions

If you pay income tax or franchise tax in multiple states, you can claim the total expense on your tax return under the SALT deduction. You’re not limited to just one state.

On line 23 of Schedule C, You may also be able to deduct the cost of registering and renewing your Certificate of Authority in each state if you operate an LLC that qualifies as a foreign entity. Since fees and renewal schedules differ from state to state, confirm with your accountant before claiming this deduction.

The home office deduction

The home office deduction allows to deduct the cost of your home office. This only applies if your home office is your primary place of work. If you rent or lease office space outside your home, you can’t claim your home office as an expense, even if you use it for telehealth sessions.

There are two ways of calculating this deduction:

- The simplified method. You claim $5 per square foot of office space, up to a maximum of 300 feet.

- The standard method. You claim a percentage of your total qualifying home expenses based on which percentage of your home’s square footage you use as office space.

It’s a good idea to calculate your deduction using both of these methods, then choose the one that offers the largest deduction.

For more on how to qualify, check out What Therapists Need to Know About the Home Office Deduction.

Telehealth software and services

The cost of any software or service you use to run telehealth sessions with your clients is tax deductible.

Your EHR may include teleconferencing functionality. If it doesn’t, the cost of any standalone software or service you use to see clients is 100% deductible.

Keep in mind that any teleconferencing solution you use must be HIPAA-compliant.

Cameras, microphones, and backdrops

The cost of any equipment you purchase in order to provide telehealth is tax deductible. That includes:

- Webcams

- Microphones

- Backdrops

- Lighting

Keep in mind that these purchases must be necessary and reasonable. For instance, a $60 microphone suitable for podcasts or streaming likely qualifies. A $2,000 condenser microphone for studio-quality recording does not.

AI scribes

AI scribes for therapists record and transcribe therapy sessions, then generate clinical notes for your files. They anonymize the data in order to comply with HIPAA requirements.

Some AI scribe tools include built-in HIPAA-compliant teleconferencing. Others are bundled with EHR platforms. The cost of any AI scribe you use in your therapy practice is 100% deductible.

EHR tax deductions for therapists

An EHR or EMR platform can help you:

- Store and track client records and progress notes

- Bill clients and file insurance claims

- Manage your schedule and make it more efficient

- Streamline client intake

Best of all, the cost of subscribing for an EHR is 100% tax deductible.

If you plan to deduct EHR costs from your taxes, be sure to keep receipts on file for all subscription payments you make.

The business meals deduction

While the Tax Cuts and Jobs Act (TCJA) of 2017 eliminated the business entertainment deduction. But it’s still possible to deduct business meals on your tax return on line 24b of Schedule C.

You can deduct 50% of the cost of a business meal:

- Shared with a business associate, employee, contractor, or potential client

- Purchased while travelling for business

- Ordered at an event you are attending for professional networking purposes

Pre-prepaired meals you buy to eat elsewhere, or ingredients for making a business meal at home, do not qualify for this deduction.

For more, check out What Therapists Need to Know About Deducting Business Meals.

The 2025 and 2026 rates for mileage deduction

If you run your own therapy practice and you drive somewhere for the purpose of work, you can deduct the expense from your taxes.

For the 2025 tax year, the standard mileage deduction was 70.5 cents per mile. For 2026, the deduction is 72.5 cents.

If you plan to claim this deduction, keep a mileage log. For each trip, it should include:

- Your departure location

- You arrival destination

- The date of departure

- The date of arrival

You’ll use that information to calculate your deduction and to back up your claim in the event of an audit.

You may also choose to calculate your deduction using the actual expenses method. That involves:

- Adding up your total miles travelled for the year

- Adding up your total miles travelled for work

- Calculating miles travelled for a work as a percentage of total miles travelled

- Deducing that percentage of your total vehicle expenses (fuel, maintenance, insurance, etc.) from your taxes.

For a complete guide, check out What Therapists Need to Know About Deducting Business Mileage.

The professional liability insurance deduction

In order to comply with licensing requirements, self-employed therapists need to carry professional liability insurance.

The cost of professional liability insurance varies, but according to Insureon, most therapists pay $800 or less per year.

The purpose of professional liability insurance is to cover your costs in case a malpractice lawsuit is brought against your practice. But it can also cover the cost of defending your license in case a complaint against you is brought to your licensing board.

For a full breakdown of how it works, check out Do Therapists Need Professional Liability Insurance?

End-of-year tax deductions

During tax season, take an opportunity to review your P&Ls and estimate your tax burden. Then, if there are any large purchases that you were planning to make next year, consider making them now in order to benefit from the tax deductions.

Your options might include:

- Annual subscriptions for software, SaaS, or web hosting that you have been paying for on a monthly basis and which you know you will use for at least one more year

- Office furniture and repairs

- New work computers, printers, or phones

- Bulk supplies (e.g. printer paper, promotional goods)

- Continuing education courses

- Subscriptions to trade or scholarly journals, or online databases

- Membership in a professional organization

Keep in mind that the cost of some tangible assets, like computers or furniture, may be depreciable. You might benefit more from depreciating them over multiple years than writing them off in the year you buy them.

—

Confused about how to maximize your deductions? Book a free consult here.

Visit our Therapist Tax Center and Tax Deductions for Therapists Hub for everything you need to know about taxes as a practice owner. If you're just starting out, here's everything you need to know about How to Start a Private Practice as a Therapist.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

Bryce Warnes is a West Coast writer specializing in small business finances.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.