Your therapy practice’s chart of accounts lists all the different ways your business earns and spends money, and tells you how to categorize each transaction.

Understanding the chart of accounts is essential for setting up a bookkeeping system for your private practice. Even if you have a bookkeeper handling it for you, understanding the chart of accounts gives you more insight into how money moves around within your business, and how your therapy practice is doing financially.

Here’s what we’ll cover:

- What is a chart of accounts, exactly?

- How do you create a chart of accounts?

- An example chart of accounts for your private therapy practice

{{resource}}

What is the chart of accounts, exactly?

You can think of the “accounts” in your chart of accounts as financial categories. While handling day-to-day bookkeeping tasks, like making entries in the general ledger and generating your financial statements, you (or your bookkeeper) refer to your chart of accounts to figure out how income and expenses should be labeled.

The chart of accounts and your general ledger

Your general ledger lists all of your therapy practice’s financial transactions, ordered by date. When a client pays you, it shows up as revenue in your general ledger. When you make a loan payment or pay rent for your office, it shows up as an expense.

If it weren’t for your chart of accounts, those transactions would be mysterious. For instance, your general ledger might show revenue of $120, but without a label on the transaction, you’d have no idea whether that money came from a client, or as royalties on a book you published.

Likewise, you could see an expense of $2,000 show up in your general ledger, and have no idea whether it was the first month’s rent in your new office, or the money you spent on new office furniture.

The chart of accounts and your financial statements

As part of regular bookkeeping, you (or your bookkeeper or accountant) draw on information in your general ledger to generate balance sheets and profit and loss (P&L) statements for your business. Each financial statement looks at different types of accounts to get the information it needs.

Broadly, your chart of accounts can be broken up into five categories:

- Assets

- Liabilities

- Revenue

- Expenses

- Equity

Some of those categories are relevant to your balance sheets, and others are relative to your P&L:

If you’re doing your own bookkeeping, you may want to label each account on your chart of accounts with the type of financial statement it appears on. That will make creating financial statements easier later on.

If you use Heard, all of this is handled for you by your bookkeeper.

{{resource}}

How to create a chart of accounts for your therapy practice

If you’re just getting started doing your own bookkeeping for your therapy practice, you’ll need to create your own chart of accounts so you can categorize all your transactions. This applies whether you’re using accounting software or a simple spreadsheet to handle your bookkeeping.

When you have a bookkeeper working for your practice, they create a chart of accounts for you.

Here are seven steps you can take to create your own custom chart of accounts for your therapy practice.

List your assets

Your assets will consist of:

- Cash in the bank

- Equipment

List all of your business bank accounts, both checking and savings. Each of these will be an item on your chart of accounts.

If you sublet a furnished office, or you’ve moved your practice 100% online, you may feel an Equipment account is unnecessary. But anything you use in the course of running your business is equipment. That includes your computer, your phone, and furniture in your home office.

If you use any of this equipment for both personal and professional reasons, a CPA or tax advisor can tell you how much of the value of each you’re able to report for the purpose of tax deductions.

List your liabilities

If you collect sales tax and need to pay it, you’ll list it here as a liability.

Otherwise, it’s mainly debts—whether student loans, or any loans you may have taken out in order to get your practice off the ground—that will appear here. Create a different account for each category of debt.

For instance, you may have a student line of credit and a student loan, but they could both be grouped under Student Loans.

Categorize your revenue

For most solo practitioner therapists, payments from individual clients are the number one source of revenue. You can name the account Client Billings or Client Payments.

If you work as an independent contractor—for instance, leading group sessions at a recovery home—you may want to break this out into a separate category, like Contract Income. That will let you track your income in more detail.

Categorize your expenses

When you create a chart of accounts for your therapy practice, the biggest task you’ll need to tackle is categorizing your expenses.

The “expense” category encompasses every way your practice spends money, covering everything from liability insurance to paper clips. For that reason, it’s likely to be the largest category on your chart of expenses.

Some expenses are recurring—like insurance payments, which are fairly easy to anticipate, because they occur regularly. Others are non-recurring, and harder to anticipate. (When are you planning to restock paperclips?)

Whether it occurs once a month or once a year, you need to categorize each and every expense, so it can be accurately entered in your general ledger.

Calculate your equity

The category “equity” includes money you’ve invested or re-invested in your business. For instance, if you set aside $5,000 of your personal assets to get your practice off the ground, and you’ve spent $2,000 of it, the remaining $3,000 will be listed as Owner Equity on your chart of accounts.

When you earn profits, any cash you don’t take as an owner’s draw or salary becomes Retained Earnings. These funds are earmarked for business use only, in order to pay business expenses or save for the future.

Label and describe every item on your chart of accounts

Once you’ve compiled items for each category in your chart of accounts, assign each account:

- A financial statement. Some accounts are relevant to the balance sheet, others relevant to the P&L. Labeling each account according to financial statement makes creating financial statements easier later on. (You can also label whole categories, ie. assets, to make it simpler.)

- A description. A brief, one-sentence description for each account helps you keep track of what’s what. And if you hire a bookkeeper later on, it will help them understand your books.

- A number (optional). You may wish to assign each account a number, which can serve as shorthand to label transactions in your general ledger. (You can see an example of how to format these numbers in the free chart of accounts below.)

Store your chart of accounts

Since your chart of accounts is static, you can create as many copies of it as you like. Typically, if you’re doing your bookkeeping with spreadsheets, it makes sense to include your chart of accounts in the same Google Sheets or Excel file as your general ledger, so you can refer to it quickly while making entries. Accounting software will store the chart of accounts for you in its own location.

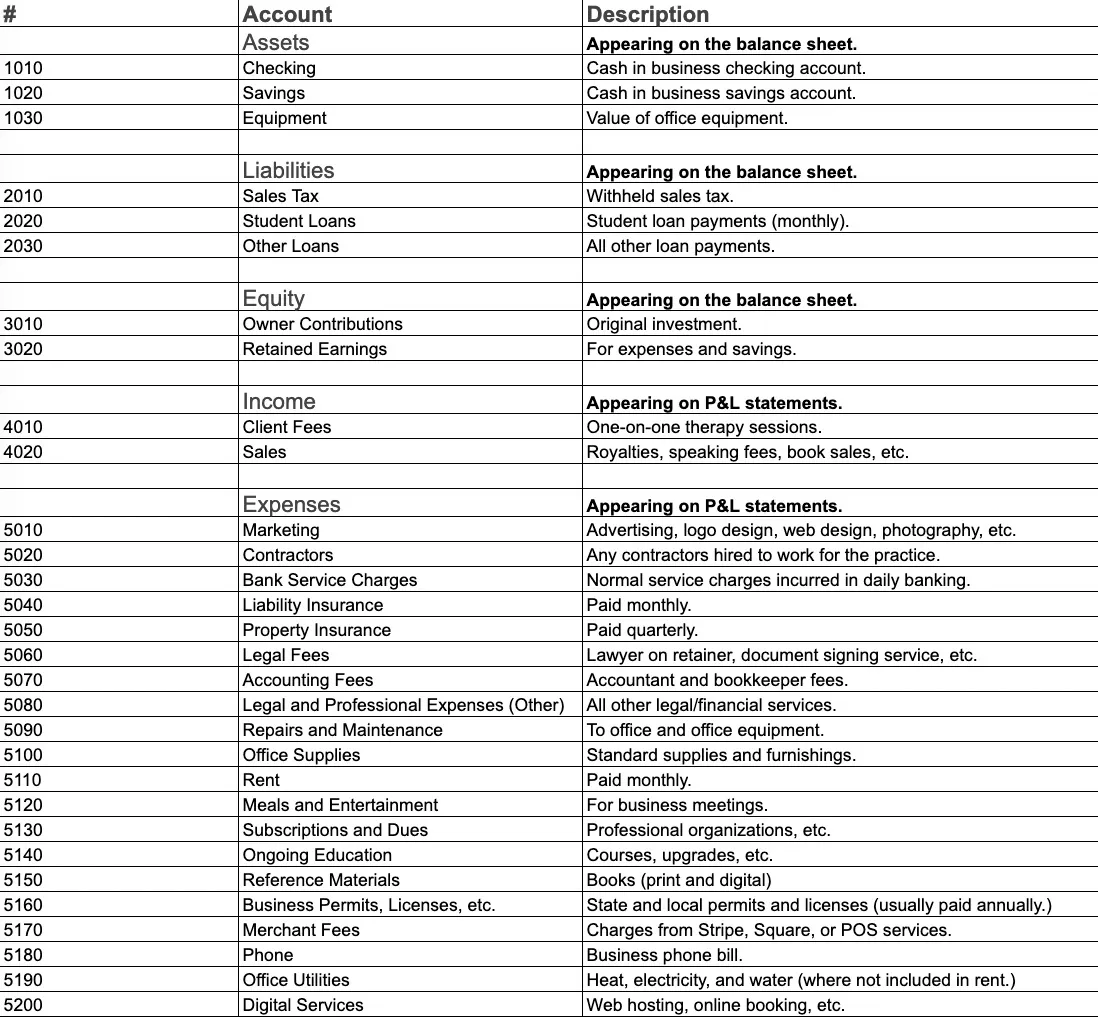

An example chart of accounts for your therapy practice

This free chart of accounts includes most assets, liabilities, revenue, expenses, and equity relevant to the majority of single person therapy practices. Click the link below to download our free template. Feel free to copy and paste it and add or remove accounts according to your needs.

{{resource}}

—

After working with over a thousand therapy practices, we’ve created the complete chart of account for therapists.

One benefit of using a chart of accounts for every business transaction? You can track deductible business expenses more easily, and reduce your tax bill. Learn about the most valuable tax write-offs for therapists.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

Bryce Warnes is a West Coast writer specializing in small business finances.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.