When you run your own therapy practice, electing S corporation status could be to your benefit.

Here’s what you need to know about therapy practices and S corporation status.

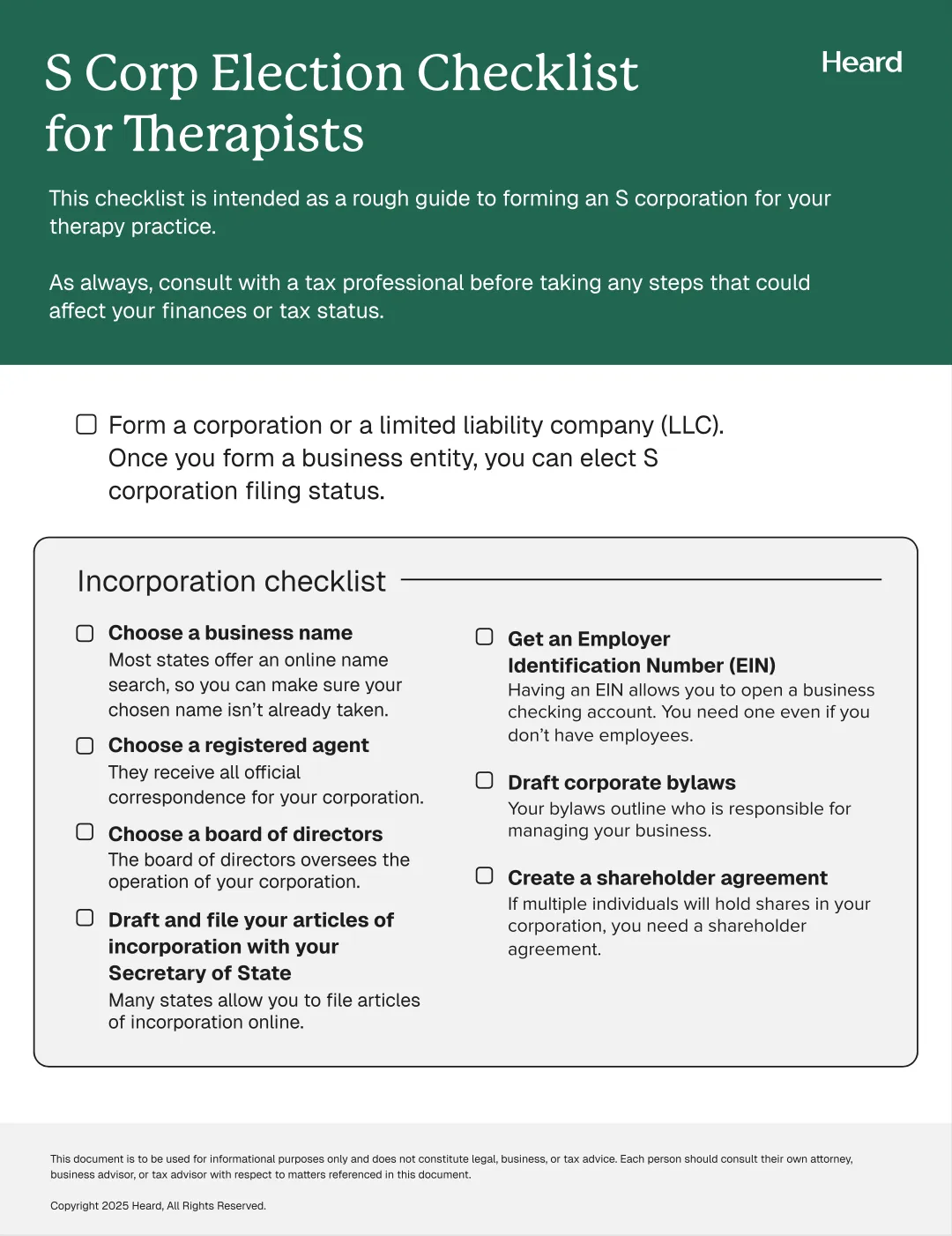

{{resource}}

What qualifies as an S corporation?

According to the Internal Revenue Service (IRS), an S corp is a corporation that has elected treatment as a pass-through entity for federal income tax purposes under Subchapter S of the Internal Revenue Code.

This tax election allows the corporation to enjoy a unique combination of benefits, so long as:

- it has fewer than 100 shareholders

- all of its shareholders are US citizens, residents, special trusts, or certain estates

- it has only one class of stock, and

- none of the members are partnerships or corporations.

Certain types of financial institutions and insurance companies are prohibited from electing Subchapter S treatment even if they meet the requirements.

Benefits of having an S corporation therapy practice

The S corporation appeals to business owners for a number of reasons.

Limited liability protection

S corporations are limited liability entities. Limited liability protects an owner’s assets by limiting the owner’s potential liability for the debts of the company to the amount the owner has invested in the company.

Although limited liability is characteristic of all corporations and limited liability companies, it does not protect the owner from liability in the case of personal negligence that results in litigation.

Also, you can lose limited liability protection if you fail to properly separate personal assets from business assets.

Pass-through taxation

Unlike most corporations, which are taxed at both the entity level and shareholder level, S corporations elect to pass corporate income losses, deductions, and credits down to the shareholders alone.

This appeals to many business owners who intend to reinvest their companies’ profits into the business. When they do, they are not penalized by being taxed at the corporate level. They are, however, still required to file annual tax returns.

Self-employment tax savings for owners

Unlike other pass-through entities, where self-employment tax is due on all pass-through income, owners of S corporations are not required to pay self-employment taxes on distributions they earn. Only their salary is subject to self-employment taxes.

Self-employment taxes consist of Medicaid and Social Security. S corporations owners do not have to pay self-employment taxes on any profits remaining after they pay themselves a “reasonable” compensation.

The Internal Revenue Code does not define what is reasonable; courts often consider what similarly situated professionals are paid in a particular region, as well as how much time and effort is required to complete the role at hand.

Qualified income business deduction

The 2017 Tax Cuts and Jobs Act allows pass-through entities to take advantage of the Qualified Business Income Deduction of up to 20 percent.

Qualified Business Income (QBI) is defined as “the net amount of qualified items of income, gain, deduction and loss from any qualified trade or business.” There are many rules and exceptions for determining the deduction. An owner must therefore carefully calculate QBI and determine how the business’s specific industry may impact eligibility and deductions.

{{resource}}

Downsides of having an S corporation therapy practice

Despite the many benefits of the S corporation, there are several limitations:

- More formalities. Although the S corporation shares many characteristics with pass-through entities, it is unable to escape corporate formalities. Annual reporting and meetings are still required.

- Increased risk of audit. S corporations may be subject to additional audits by the IRS aimed at identifying abuse when it comes to avoiding self-employment taxes. These examinations often focus on determining whether an owner underreported the owner’s “reasonable” salary to avoid taxes.

- High cost. In many jurisdictions, the cost of forming a corporation exceeds that for forming other entity types. An owner could incur the additional cost, but then find that its business profit model does not afford it all of the S corporation benefits.

Taxes and your S corporation therapy practice

S corps must file Form 1120S, U.S. Income Tax Return for an S Corporation, on an annual basis, to report income and deductions. Each shareholder of the S corp receives a copy of Schedule K-1 (part of Form 1120S), Shareholder's Share of Income, Credits, Deductions, etc.

Income, loss, and credit items "flow through" to the shareholders on a per-share basis. Form 1120S records the ordinary income of the S corporation. Separately stated items, those that could be taxed differently to the various shareholders, are reported on Schedule K-1 of the 1120S.

S corps are pass-through entities and generally do not pay a corporate-level income tax on corporate income as do C-corporations. Rather, income is treated as if it were directly earned by the shareholders, who are then taxed on their pro rata shares of the corporate earnings even if the earnings are not distributed.

How to file taxes for your S corporation therapy practice

In order to file Form 1120S, you’ll need the following information on hand:

- Your gross income

- Expenses you will deduct

- Names and addresses of all persons owning stock in the corporation

- The number of shares of stock owned by each shareholder

- The amount of money and other property distributed during the year by the corporation to each shareholder and the date of each distribution

- Each shareholder's pro rata share of each item of the corporation for the tax year (Schedule K-1)

- Any additional information required by Form 1120S that may apply in your circumstances

What is the filing deadline for my S corporation's taxes?

Returns for S corps must be filed no later than the 15th day of the third month after the close of the S corp’s tax year, or March 15 for those using the calendar year. You can file electronically or by mail. You can file a six month extension if need be.

States vary in their recognition and treatment of S corps. While there are clear advantages to having an S corp, you should pay close attention to the myriad of state-level variances that ultimately impact your tax filings and obligations.

—

Not sure you’re ready for the leap to an S corporation? Learn all about tax basics for sole proprietorships.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.