Key takeaways

- Therapists prepare superbills for clients, who then file them with their insurance companies to claim out-of-network benefits

- After a claim is approved, an insurer reimburses the client for a portion of the cost of therapy

- Making sure your superbills are accurate and delivered on time increases the likelihood clients will be reimbursed

A superbill is a receipt out-of-network therapists create for their clients. The client submits the superbill to their insurer. If they have out-of-network benefits, and if their insurer approves the claim, the client is reimbursed part of the cost of treatment.

At least 55% of Americans with employer-sponsored health insurance have out-of-network benefits. Many of them rely on out-of-network benefits in order to afford seeing their therapist of choice. By providing clients accurate, timely, and correctly formatted superbills, you make therapy more accessible to them and improve client retention.

Here’s everything you need to know to create superbills for your therapy practice.

What is a superbill?

A superbill is absolutely essential for any therapy client who wants to claim out-of-network benefits. It lists all the treatment the client has received within a given period, including its cost. Once they submit a superbill to their insurance company, the insurer uses the information on the superbill to determine whether to cover the claim.

Contrast this with typical in-network insurance claims:

- You have a contract with a particular insurance company indicating that you will provide services to enrolled clients

- You—not your client—submit claims to the insurance company

- The insurance company reimburses you at an agreed-upon rate

Out-of-network benefits put the responsibility for filing claims in the client’s hands, not the therapist’s. And the client needs an accurate superbill in order to submit their claim.

How do you submit a superbill to insurance?

As a therapist, you do not personally submit a superbill to a client’s insurer. It’s up to the client to submit the superbill when filing a claim for out-of-network benefits coverage.

What information is included on a superbill?

A valid superbill includes:

- Client information, including their full name, date of birth, plan membership number, group insurance number, and address

- Therapist information, including your full name, credentials, NPI number, taxonomy code, practice address, and contact info

- Session details, including the date of each session, relevant CPT codes, and fees charged

- Diagnosis codes, indicating the client’s diagnoses using ICD-10 (most clients must have formally diagnosed conditions in order to use out-of-network benefits)

- Total amount paid by the client

- Your tax ID and signature—these aren’t always necessary, but some providers do require you to provide an SSN or EIN and sign the superbill

How do you create a superbill?

You can draft a superbill by hand using your own template.

EHR software that includes support for billing and insurance claims also typically includes tools for generating superbills. The benefit of these systems is that they sync with client records, so you may be able to automatically import client information without entering it by hand.

How does a client get reimbursed with a superbill?

When they use out-of-network benefits, a client pays you 100% of your fee upfront. Up to that point, they’re treated exactly like a cash pay client.

Once they’ve paid, you provide the client a receipt in the form of a superbill. The client then submits the superbill to their insurer.

Four important points to note about client reimbursement:

- Cost sharing only starts after they meet their deductible

Until they meet their deductible for out-of-network benefits, the client pays out of pocket. Once they meet their deductible, their insurer starts sharing costs (in the form of reimbursement).

Out-of-network deductibles are typically 2 to 3 times higher than in-network deductibles. But they usually apply across different forms of treatment. For instance, if a client sees a physiotherapist, a nutritionist, and a therapist who are all out-of-network, the total amount they pay for all treatments counts toward their out-of-network deductible.

- Reimbursement is based on the insurer’s allowed amount

As part of a contract with an enrolled individual, each insurer sets allowed amounts for specific types of treatment (typically based on CPT code). This is the maximum amount the insurer will cover.

Clients are reimbursed a portion of this allowed amount. For instance, a client may receive 70% of the allowed amount in the form of a reimbursement. The remaining 30% is coinsurance (money they pay out of pocket).

The allowed amount for treatment may be less than your hourly rate. For instance—following the previous example—if your hourly rate is $175, but the insurer’s allowed amount for out-of-network therapy is $120, your client will only be reimbursed 70% of $120.

- They need to wait to be reimbursed

Reimbursement is not instantaneous. In a best case scenario, a client should expect to wait two to three weeks before being reimbursed by their insurer. More typically, the wait is four to six weeks. And if the claim is flagged for review, they may wait up to twelve weeks.

Claims submitted electronically, with direct deposit set up, are usually the fastest to be reimbursed. That’s particularly the case with larger insurers who may have more efficient out-of-network processing.

- Mandated out-of-pocket maximums do not apply

Federally mandated out-of-pocket maximums for health insurance do not apply to out-of-network benefits. Insurers typically set much higher out-of-pocket maximums for out-of-network care, and many do not have maximums at all.

Which clients need superbills?

Any client who wants to be reimbursed for therapy by using their out-of-network benefits needs a superbill.

Three types of health insurance provide out-of-network benefits:

- Preferred provider organization (PPO) plans

- Point of service (POS) plans

- High deductible health plans with savings options (HDHP/SOs)

Of those, PPO and POS plans always include out-of-network benefits.

An HDHP/SO may or may not come with out-of-network benefits. An HDHP/SO is structured like any typical insurance plan, with two key differences:

- It has a higher deductible and lower premium than typical plans

- It includes a savings option (a health savings account (HSA), flexible spending account (FSA), or health reimbursement arrangement (HRA)) to help offset the high deductible

If a client’s HDHP/SO is structured as a PPO or POS, they likely have out-of-network benefits. If it’s structured as any other type of plan, they most likely do not.

According to the 2025 Employer Health Benefits Survey, 46% of workers with employer-sponsored health insurance had PPO plans, 33% had HDHP/SOs, and 9% had POS plans.

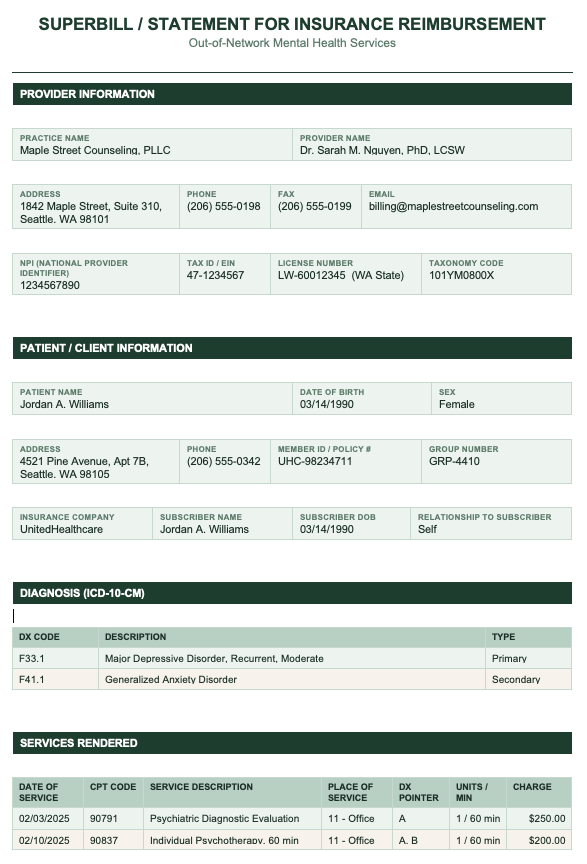

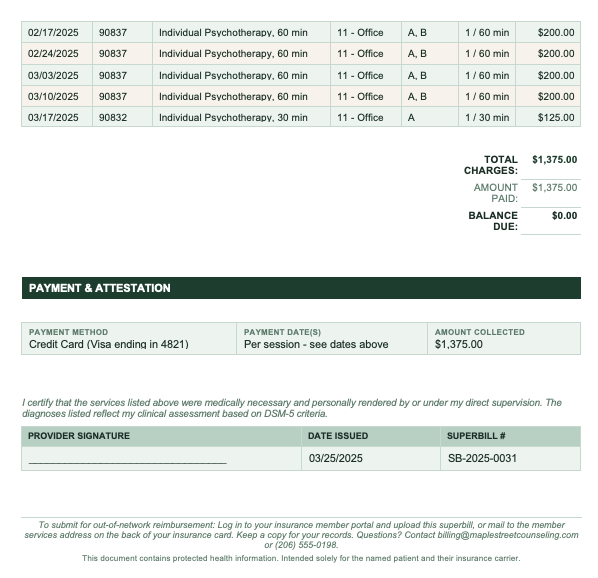

What does a superbill look like?

Here is an example of a superbill for multiple therapy sessions:

The format of a superbill depends on which software or template you use to generate it. But this example includes all the required information laid out in a way that makes it easy for an insurance company to process it.

What is the filing deadline for a superbill?

Different insurance companies set different filing deadlines for superbills. Some insurers give members up to 90 days after receiving treatment to submit superbills, while others may give them up to 365 days. Your client can check their deadline by reviewing their insurance policy paperwork.

How do clients submit superbills?

Most large insurers provide online portals where clients can submit superbills. They may also be able to submit superbills via their employer’s HR platform.

But in some cases, a client may need to submit a superbill by mail. They can find the mailing address for out-of-network claims in their policy paperwork.

What is an explanation of benefits (EOB)?

An EOB is a document an insurer sends to a member after they have claimed out-of-network benefits.

The EOB includes:

- The total fee for treatment

- The allowed amount covered by insurance

- The portion of the allowed amount reimbursed by insurance

- The coinsurance paid by the client

- The total remaining deductible for out-of-network benefits

If the client hasn’t paid down their out-of-network deductible, the remaining deductible will be adjusted and the amount reimbursed will be listed as $0.

Why are superbills denied?

An insurer may reject a superbill submitted by a client to claim out of network benefits if:

- Provider information is missing or incorrect. That applies to tax IDs, NPIs, and taxonomy codes. In particular, your taxonomy code (specifying your credentials) must match the CPT codes (indicating what type of treatment you provided).

- Diagnosis and procedure codes don’t match. All CPT codes need to be clinically consistent with the client’s diagnosis, which is designated by an ICD-10 code.

- Member or group information is missing or incorrect. The member code designates a particular member of a plan, and the group code designates the sponsor (typically the member’s employer).

- The filing deadline has passed. If the superbill is filed after the deadline set by the insurance company, the claim will most likely be rejected.

- Services are not covered. Some out-of-network benefits exclude therapy. Others limit claims to treatment for specific diagnoses.

- A duplicate has been submitted. If the client submits the same superbill twice, or if you bill insurance for the same treatment as an in-network provider and the client then submits a superbill, it will be rejected.

You can reduce the likelihood a superbill will be rejected by:

- Double-checking that all information is complete and accurate

- Making sure taxonomy codes and ICD-10 codes match up with CPTs

- Ensuring your client has accurate information about their coverage (eg. extent of out-of-network benefits)

- Encouraging your client to submit before their filing deadline

What happens if a superbill is denied?

If an insurer rejects a superbill submitted by a client, they are required to explain the reason on the EOB. There are different approaches a client can take depending on the reason for denial.

Clean claim issues make up the majority of denials. They’re caused by incorrect or missing information such as a member ID or provider NPI. These types of denials do not need to be appealed. You simply prepare a new, corrected superbill and the client can resubmit it.

Substantive denials occur when an insurer determines that treatment is not medically necessary, that the service is not covered, or that—based on your credentials—you are not an eligible provider. These must be appealed. The insurer is required to tell the client how to appeal and give them a deadline. Under ACA rules, this is typically 180 days after the EOB date.

A strong appeal should include:

- A letter of medical necessity from you, the treating provider

- Clinical notes to support the treatment or diagnosis

- If the denial seems inconsistent with the policy terms, a written argument citing the plan’s own language

If an appeal is denied, the client can request an external review. For most plans, federal law gives members the right to request an independent review carried out by a third party not affiliated with the insurer.

Are superbills protected by HIPAA?

Yes, all superbills include protected health information (PHI), so they are subject to HIPAA.

When you create a superbill for a client, you must store and transmit it using HIPAA-compliant software. That includes email: Emailed superbills should be via a platform that provides a business associate agreement (BAA) covering HIPAA requirements.

If you use an EHR platform to generate superbills, it is almost certain to be HIPAA-compliant already. But any superbills you print; or generate, export, and then attach to an email, must be shared according to HIPAA requirements.

How can you make superbill reimbursement faster?

To some extent, clients’ reimbursement times for out-of-network benefits are out of your control. Insurers have their own internal processes, and certain insurers—particularly larger companies—are faster at processing claims.

But there are steps you can take to increase the likelihood a client will be reimbursed ASAP:

- Provide a timely superbill. Generating a superbill within 24 hours after a client pays puts it in their hands as soon as possible, so they can submit their claim before the filing deadline.

- Collect insurance info at intake. If a new client is planning to use out-of-network benefits, gather necessary insurance information at intake. That includes their membership and group numbers and their diagnosis codes.

- Request prior authorization in advance. Prior authorization is typically only necessary for in-network claims, but some providers require it for out-of-network claims as well. If necessary, request it as part of the intake process for new clients.

- Automate your superbills. Using an EHR platform or other HIPAA-compliant superbill tool lets you pre-fill form fields and automatically import client info, reducing the likelihood of errors leading to claim denial.

How can therapists automate the superbill process?

Instead of your clients needing to submit superbills to their insurance, which can be time consuming for them, you can use an out-of-network billing solution like Thrizer or Mentaya. When you bill a client through one of these tools, a superbill is automatically submitted to their insurance company, removing the client completely from the process. They will even deal with the insurance company on your client's behalf if a claim gets denied or further action is needed.

Summary

- In order to claim out-of-network benefits, a client needs you (their therapist) to create a superbill, which they then submit to their insurer

- Insurers can take from two to three weeks to twelve weeks to process claims and reimburse clients

- Reimbursement amounts are based on the insurer’s allowed amount for therapy, not necessarily on your hourly rate

- Claims are most commonly denied due to missing or incorrect information on superbills, or even typos; corrected claims may be resubmitted without making an appeal

- If a superbill is rejected for substantive reasons—like the insurer not covering the treatment—then the client can request an appeal

- EHR platforms often include tools that make generating superbills faster and less prone to error

- Superbills include PHI, and they’re subject to HIPAA requirements

For a deeper dive, check out our Complete Guide to Out-of-Network Billing for Therapists.

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.