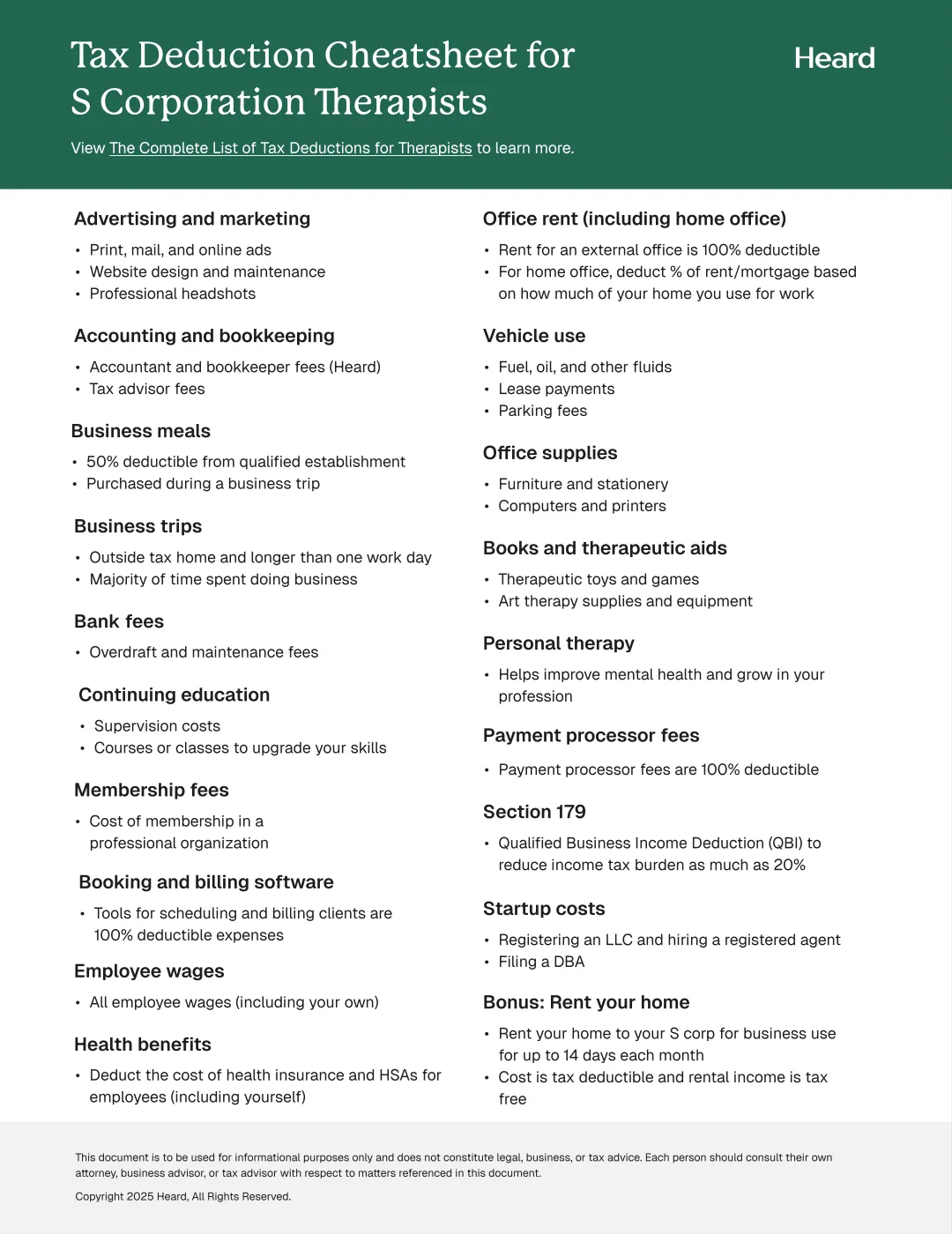

S corporation status offers your therapy practice a variety of benefits.

That includes the opportunity to reduce your practice’s tax burden. When you pay less in taxes each year, you have more money to reinvest in your practice.

Here are six smart business moves you can take to start saving on taxes ASAP as an S corporation therapy practice.

{{resource}}

Take advantage of S corp distributions

When your practice is an S corporation—and you’re an employee—you receive income in two forms:

- Salary, processed by payroll, with taxes withheld (federal and state income tax, FICA, etc.)

- Distributions, taken from the S corp’s profits and reported on Schedule K-1

When you earn income as a sole proprietor, all profits are subject to a self-employment tax of 15.3% (paid in lieu of FICA).

With an S corp, however, you don’t pay self-employment tax on the S corp’s overall profit (including the portions you receive as distributions). Instead, you pay FICA on your salary only.

You can save significantly on your taxes by taking as much of your income as possible in the form of distributions. In fact, this is one of the main reasons therapy practices elect S corporation status—to avoid paying self-employment tax on 100% of their income.

Here’s the catch: The IRS requires you to pay yourself a reasonable salary as a therapist. They don’t want you paying yourself a tiny salary while taking most of their income as distributions, thereby dodging self-employment tax or FICA.

What’s more, the IRS won’t tell you what a reasonable salary ought to be. However, by consulting our article on reasonable salaries for therapists, and talking to a qualified CPA or tax advisor, you should be able to hit the magic number. And that means maximum self-employment tax savings thanks to income in the form of distributions.

For a deeper dive, check out our article on tax basics for S corporation therapists.

Claim the QBI deduction

The qualified business income (QBI) deduction can reduce your income tax burden by up to 20 percent. And while any pass-through entity—including sole props—can qualify for this deduction, S corps are at a special advantage.

That’s because the QBI deduction only applies to self-employment income, not wage earnings. If you set a low (but acceptable, to the IRS) salary for yourself, and also claim the QBI deduction, your self-employment income (in the form of distributions) not only benefits from saving on self-employment taxes (at a rate of 15.3%) but enjoys a 20% QBI tax reduction.

Contrast this with a sole prop, which must pay self-employment tax on 100% of its income before applying the QBI deduction.

There’s an income threshold you must fall under in order to qualify for the whole 20% deduction; above that threshold, your income is only partially eligible for Q BI. Even so, it can result in substantial savings for your practice.

Get the full how-to from our guide to the QBI deduction for therapists.

Rent your home office to your S corporation

This one is a bit tricky—expect extra paperwork—but it could save you a considerable chunk of change in taxes.

It works like this: You rent out a portion of your home to your business for meetings. The cost of the rental is tax deductible (for your S corp), and the money your S corp pays you (an individual) is tax-free income.

If you work entirely from home, check out the home office deduction for therapists.

At maximum, you may rent out your home to your practice for 14 days out of every year. The rental must be for the purpose of business meetings, not entertainment.

For the full breakdown, check out this article on the Section 280a deduction.

There may be other caveats; make sure you check state laws regarding commercial rentals and home-based business activities, and consult with a CPA if necessary.

Hire your kids

If you have children, you may be able to hire them in order to reduce your tax burden.

Common sense says that a toddler isn’t prepared to serve as your new office administrator, and a seven-year-old isn’t ready to start clocking clinical hours. But if your kids are old enough to handle certain tasks for your S corporation—whether it’s tidying the office or managing your TikTok account—then you can hire them to work for you.

A family member working for your business can earn up to $12,000 annually before their wages are subject to federal taxes. Just make sure they’re on payroll, and that you record their work hours, earnings, and duties on the job.

And whether or not you keep wages below the $12,000 threshold, any wages you pay out are tax deductible business expenses.

There may be laws at the state level that affect the ability of young family members to work for your practice. And it’s important to make sure you have all your boxes checked off before you cut the first paycheck. Talk to a CPA before making any hiring decisions.

Check out our article, Can I Hire Family Members to Work at my Therapy Practice?

Cover your own health insurance premiums

When your S corporation covers employees’ health insurance premiums, it’s a deductible business expense. And, since you are an employee of your S corporation, you may be able to pay your own insurance premiums (or reimburse them) and write off the expense.

Importantly, you’re only eligible for this write-off if you don’t have a spouse who has healthcare coverage available through their employer.

But if your practice’s health benefits are your family’s only option for employer-subsidized health insurance, then you’re good to go. Coverage through your S corp can cover you, your spouse, and your dependents. File the expense as a self-employed health deduction on Form 1040.

You can learn more from our complete list of tax deductions for therapists.

Set up a solo 401(k)

If you’re the only employee of your S corp, you intend to save for retirement, and you would also like to reduce your practice’s tax burden, a Solo 401(k) is the way to go.

Income you contribute to your 401(k) is untaxed at the time you contribute. Income tax is applied later, when you withdraw funds—ideally after retirement, when you are in a much lower tax bracket.

Contributions may come both from you as a wage-earner and from your practice as a separate business entity.

To learn more, check out our article on how to choose a retirement plan for your therapy practice.

—

Looking for more strategies to help your S corp therapy practice succeed? Check out our complete guide to S corporations for therapists.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

Bryce Warnes is a West Coast writer specializing in small business finances.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.